|

|

|

|

Dáil Éireann An Coiste um Chuntais Phoiblí An Chéad Tuarascáil Eatramhach,2007 Rochtain ar an Eilimint Phríobháideach de Chomhpháirtíochtaí Poiblí Príobháideacha – Comparáid Idirnáisiúnta Márta, 2007 Dáil Éireann Committee of Public Accounts First Interim Report, 2007 Access to the Private Element of Public Private Partnerships – An International Comparison March, 2007 (Prn. A7/0396) Contents

Chairman’s Preface This report of the Committee of Public Accounts (PAC) is concerned with parliamentary scrutiny of the private aspect of public private partnerships entered into by State bodies. The scrutiny of PPPs is an issue that the Committee first commented on in an interim report published in May 2005. Specifically, the Committee recommended that:

The Minister for Finance, through his ‘Minute’ to the Committee, replied in July 2006 that he is “satisfied that (current) arrangements are adequate to facilitate parliamentary oversight of PPPs.”. The Committee, having discussed the ‘Minute’ of the Minister, decided that the matter warranted further examination and to that end appointed Deputy Dan Boyle to act as rapporteur to prepare a draft report for its consideration. This is the conclusion of the Committee’s consideration of the report prepared by Deputy Boyle. The Committee recommends this report to Dáil Éireann.

Michael Noonan, T.D., Chairman. March, 2007 Members of the Committee of Public Accounts FIANNA FÁIL

FINE GAEL

LABOUR

GREEN PARTY

SOCIALIST PARTY

1 Deputy Michael Noonan replaced Deputy Padraic McCormack by order of the House on 18th June, 2003. 2 Deputy John Deasy replaced Deputy Paul Connaughton by order of the House on 20th October, 2004. 3 Deputy Tom Hayes replaced Deputy John Perry by order of the House on 20th October, 2004 Deputy Michael Noonan elected as new Chairman on 21st October 2004 4 Deputy Michael Smith replaced Deputy Batt O’Keeffe by order of the House on 16th November, 2004. 5 Deputy Joan Burton replaced Deputy Pat Rabbitte by order of the house on 29th November, 2005. Orders of Reference of the Committee of Public Accounts

The Report Section 1 Introduction and Background to this Study1.1 DefinitionThe term “public-private partnership” (PPP) has been in general use since the 1990s. However, there is no widely agreed, single definition or model of a PPP. The term PPP covers a range of different structures where the private sector delivers a public project or service. Concession-based transport and utilities projects have existed in EU member countries for many years, particularly in France, Italy and Spain, with revenues derived from payments by end-users, e.g. road tolls. The UK’s Private Finance Initiative (PFI) expanded this concept to a broader range of public infrastructure and combined it with the introduction of services being paid for by the public sector rather than the end-users. The use of PPPs has now spread to most EU member countries and depending on the country and the politics of the time, the term can cover a spectrum of models. These range from relatively short term management contracts (with little or no capital expenditure), through concession contracts (which may encompass the design and build of substantial capital assets along with the provision of a range of services and the financing of the entire construction and operation), to joint ventures and partial privatisations where there is a sharing of ownership between the public and private sectors. 1.2 Off-Balance Sheet Treatment of PPPsOne of the reasons for the popularity of PPPs with governments is the fact that under Eurostat guidance or local accounting rules, many PPP transactions can be classified as off the public sector’s balance sheet. This means the authority will only account for the annual payments it makes to the PPP company, and not for the assets and liabilities of the project, including its debt. The off-balance sheet treatment of PPPs is attractive in so far as long-term obligations under PPPs do not appear under governments’ overall budgets. Annual government budgets show instead the annual payments for the services received, thereby helping to keep government deficits within the reference value of 3% of GDP, as per the Stability and Growth Pact adopted in 1997 to strengthen the Maastricht Treaty provisions. As a corollary of this, the public may not be adequately informed of the true condition of the State’s finances. This leads to a lack of accountability. Alternatively it is also argued that the value of PPPs in terms of financial relief to the Exchequer is more than just an accountancy issue. PPPs can relieve Exchequer spending not just nominally, but also substantially, by balancing budgets and reducing public debt. The underlying economics argument here is that in many European economies, public sector investment has been crowding out private sector investment for many years. PPP is a means of substituting public sector investment (and hence debt) for private sector investment (and hence debt) in a manner that is still directed by central government. The issue of financial relief to the Exchequer should be taken into particular account in making cross-country comparisons involving Ireland, as we have a much lower level of Debt-to-GDP than other European countries where the PPP model is gaining currency. At the same time, our level of private debt is alarmingly high. Thus, one of the main reasons for turning to PPP in countries such as Germany does not currently apply to Ireland and raises questions about an increasing use of financially driven PPPs in this country. The current stated position of the Department of Finance is that, on a case by case basis, the decision to opt or not for a PPP solution is governed solely by value for money considerations. 1.3 Accountability IssuesPPPs provide public infrastructure in many areas of life, from schools to roads and prisons. However, the full details of many such projects, often large-scale and high profile have not been subject to public scrutiny. This has caused some disquiet among commentators and public representatives charged with keeping a watchful eye on public spending. In particular, the excessive use of “Commercial-in-confidence clauses” (the private entity’s cost structure and profit margins) prevents the full disclosure of details such as the value for money comparison and the expected return on investment. The alternative argument is that PPPs, by making a particular investment project subject to market forces, may be automatically creating a kind of market accountability which is absent in traditional forms of public sector investment. Where consumers pay to use a service, the quality of the service will affect profitability, making the operator automatically accountable to the service users by means of the profit motive. The extent to which this is the case will depend on the degree of competition and whether the service is a necessity or a luxury. PPPs that put into place monopolies for necessity services (e.g. waste collection) will be less subject to market accountability than those for competitive, luxury services (e.g. a concession to run a motorway rest stop). In this way, investment in the railway network could increase the effectiveness of road transport PPPs by enhancing the market accountability mechanism. The mechanisms of market accountability and public accountability can to some extent be mutually compatible: Monopoly PPPs require public accountability because these markets don’t function. But in these cases there is less of a justification for a commercial confidentiality clause, which seeks to protect market-sensitive data from competitors. Against this, PPPs in competitive sectors may require commercial confidentiality, but at least offer market accountability through the mechanism of the market. The Public Accounts and Estimates Committee of Victoria (Australia) stated in its report on Commercial in-Confidence Material and the Public Interest:

George Monbiot, a well-known and acknowledged critic of PFIs in the UK put it like this:

1.4 Access to Information on the Private Element of PPPsPublic Private Partnerships have been playing an increasingly important role in Ireland. The transport and water and waste sectors have seen the most activity to date within Ireland, with the most deals closed and in procurement. In particular, there have been four road PPP projects closed in the past five years with a further six in procurement, including the €400m N6 Galway to Ballinasloe road PPP contract. The role of the National Development Finance Agency (NDFA) was redefined to include responsibility for the procurement of all new PPP projects in the central government area (with the exception of road and rail). The Government has also announced a series of new PPP projects in the courts/prisons, health and education sectors and has set specific targets for projects financed through PPPs. There are 73 PPP projects on the NDFA’s most recent list, ranging from roads, courts, school building and refurbishment, sewage treatment plants, prisons, light rail, residential re-development and drainage. However, limited parliamentary access to key information on major PPP contracts has diminished accountability of Government to the Dáil. In May 2005, the Public Accounts Committee (PAC) recommended that:

The Minister for Finance responded in his ‘Minute’ to the Committee: “As regards Parliamentary oversight of PPPs, the Minister notes the oversight on individual Ministerial portfolios exercised by the relevant Select Committees of the House, who may examine all issues within the ambit of Ministers. In addition, he notes the current powers of the Committee as set out in legislation and in its terms of reference. He also notes that all PPP projects are subject to examination by the Comptroller and Auditor General. All documentation held by State authorities entering into PPP projects is fully available for review by the Comptroller and Auditor General for reporting by him, as appropriate, whether these relate to PPP projects funded by Exchequer unitary payments or projects funded by user charges. Arrangements for VFM examinations by the Comptroller and Auditor General have provided access to a substantial amount of relevant information, including the financial model used by the winning bidder in the PPP arrangement. The financial model includes the discounted cash flows for the project, based on the risk transfer to the private sector consortium reflected in the project contract and also includes information on the internal rates of return on private sector investment in the project. This access is illustrated by the VFM report on the Bundled Schools project. The Select Committees of the House and the Committee of Public Accounts can request documentation from State authorities in the course of its proceedings and the Minister expects that authorities would respond positively to such requests, addressing, where relevant, considerations of commercial sensitivity or confidentiality and of legal professional privilege. Expenditure in relation to PPPs remunerated by unitary payments is presented in a separate Subhead in the Estimates, which facilitates consideration by the relevant Select Committee. These are in turn accounted for in the relevant Appropriation Accounts and the relevant Accounting Officer may be required to give evidence to the Committee in relation to these. The Minister is satisfied that these arrangements are adequate to facilitate Parliamentary oversight of PPPs.” Following this response, the Committee decided to investigate the way in which similar projects are dealt with in other jurisdictions and has undertaken to conduct a comparative study so that it would be in a position to make firm recommendations, based on international best practice. To this end contact was made with EUROCONSTRUCT contacts in 19 European countries. However, it was found that many construction experts are not at all familiar with the finer detail of accountability of the PPP vehicle. It was also decided that it was probably most instructive to look at the countries with the most developed PPP portfolio, namely the UK, Australia and Canada. The Australian experience was found to be particularly educational. The PAC in recent years has held several plenary sessions relating to significant PPP projects. These meetings of the committee were informed by particular chapters of the annual reports of the Comptroller and Auditor General, as well as a number of Value For Money reports that also emanated from his office. Among the projects examined have been

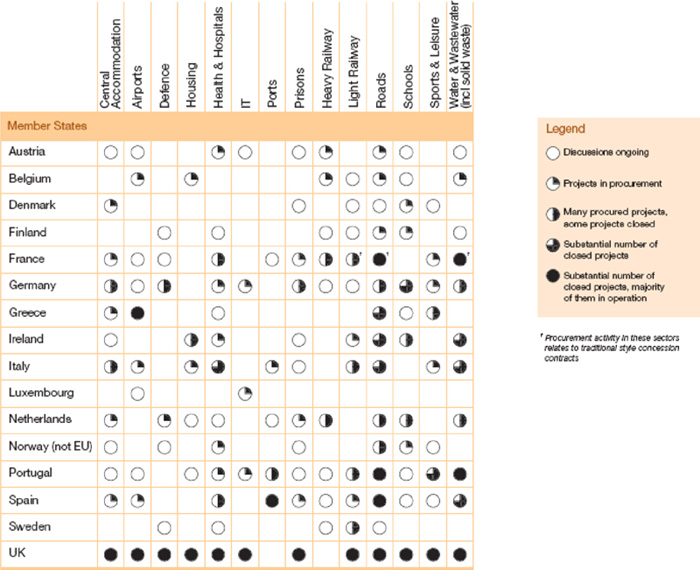

While the circumstances applying to each of these projects vary widely, and the history of each differs, some common threads have appeared. The largest common factor has been the frustration expressed at the Committee of either not having appropriate access to information relating to these projects, or being publicly unable to refer to information deemed to be commercially sensitive. This committee believes that this obstacle needs to be overcome. Public accountability and value for money are very important issues. It should be noted that the National Development Finance Agency (Amendment) Bill 2006 is currently proceeding through the Houses of the Oireachtas. If enacted it would provide a statutory framework for the oversight of many PPP projects. This report outlines further approaches to oversight that exist in other jurisdictions and should also be adopted here. Section 2, sets the scene by briefly looking at the PPP experience in Ireland and in selected countries in Europe and beyond. In Section 3, examines the access to the private aspects of PPPs to PACs in a number of countries. Section 4 contains draft recommendations, including suggestions for future study. Section 2 PPP Experience in Ireland and Selected other Countries2.1 European PPP ExperienceIn 2004 and 2005, around 206 PPP deals worth approximately US$52 billion/€42 billion were closed in the world, of which 152 projects with a value of US$26 billion/€21 billion were in Europe (in this case referring to the EU Member States, the EU acceding countries (Bulgaria and Romania), the EU candidate country Turkey, and Norway). From January 1994 to September 2005, it is estimated that PPP deals with a value of approximately US$120 billion/€100 billion closed across Europe. Of these deals, two thirds closed in the UK, with the other PPP hotspots of Spain and Portugal accounting for 9-10% each. The UK showed substantially more PPP activity than the rest of Europe with 118 deals closed in 2004 and 2005, with the next most active PPP market – Spain – closing 12 deals during the same period. The first chart shows the state of PPP development in the EU 15 countries. Many countries start using PPPs in the provision of road infrastructure, moving on to their use in other sectors, such as water and waste treatment, education, health, energy. The chart shows that roads and water and wastewater were the most frequently used sectors across the sample of countries. These are the two sectors where Ireland has a substantial number of closed projects. The UK is the most advanced country with respect to PPP (PFI) use, having substantial numbers of closed projects, the majority of them in operation. PPPs in EU 15 Countries

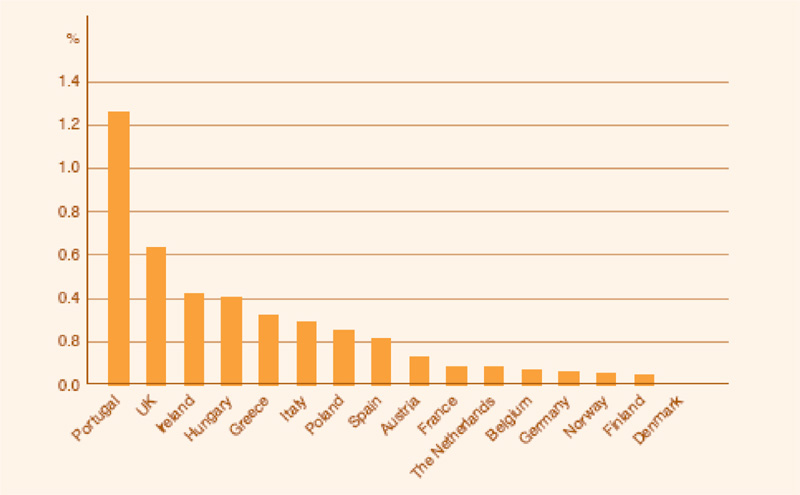

While the UK closed the greatest number of PPP deals in 2000-2005, if PPP activity is considered as a percentage of GDP, Portugal has the greatest involvement with PPPs relative to its GDP, with Ireland ranking third. Hungary and Greece also have high levels of PPP usage relative to Gross Domestic Product as the next figure shows. Average 2000-2005 PPP Activity as a Percentage of Mean GDP

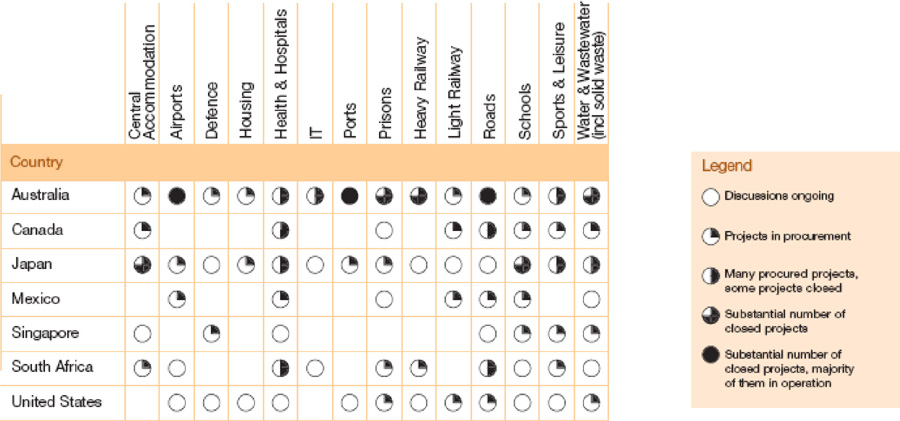

In the Coalition Agreement document of 2005, the German Federal Government’s coalition partners CDU/CSU and the SPD agreed to introduce new legislation in early 2007 to facilitate new PPP projects and simplify the bureaucratic process, for which a PPP Task Force was set up by the Government. A vote on the new legislation is planned for April 2007. However, concerns have arisen among the President and Vice President of the Courts of Auditors at how the PPP procedure is currently being handled, in particular in relation to what long-term risks and obligations were presented to the Exchequer by PPP investments. On foot of this a Parliamentary Question was asked on 12/02/2007 detailing concerns about the degree of transparency. No response from the Government has yet been made. (Source: German Bundestag; 2006 Annual Report of the Bundesrechnungshof) 2.2 Outside Europe: PPP Experience in Australia, Canada, JapanThe chart shows that Australia is one of the most advanced countries with respect to the use of PPPs, having substantial number of closed and operational projects in the airports, ports and roads sectors. Prisons and water and wastewater projects are also very advanced. Japan has concentrated its PPP projects in the sectors of central accommodation (i.e. government offices) and schools. The United States by contrast have only reached procurement stage in the prisons, light railway and water & wastewater sectors, with most other sectors at ongoing discussions stage. PPPs in Non EU Countries

Section 3 Public Accountability of PPPs – International ExperienceIntroduction:The monitoring of PPPs takes place at several levels. The fundamental level is the relationship between the public sector’s operational team – say from within the Department of Health and the private company. Recent studies on operational PPPs and PFIs in the UK have found that authorities were surprised by the level of input required of them in contract monitoring. It was frequently seen as substantially higher than had originally been anticipated. This was both in terms of the local authority team and also with users (e.g. in schools by school staff). Respondents to a survey by PUK questioned whether this level of resource was sustainable over the typical 25 year life of a contract. Since most projects operational in the UK at the moment have only been up and running for a few years, it is not yet clear if these concerns will be borne out. The former Auditor-General of the State of Victoria in Australia indicated that he was concerned about the ongoing oversight and monitoring arrangements for PPPs, and the potential to lose corporate memory over the life of the contract:

To address community concerns about the lack of transparency and accountability of PPP projects, most governments have strengthened governance processes and systems for evaluation and review. Given that corporate memory tends to be short term, it is of particular importance that elected representatives are fully informed and have access to all relevant information. However, the access to Commercial-in-confidence information by public representatives and the public still remains a contested issue. Below is a summary of the mechanisms for public accountability in place in a number of countries which have had considerable experience with PPPs. 3.1 United KingdomThe UK has continued to widen its use of PPPs across a number of sectors. According to UK Treasury figures, over 450 deals with a value of more than £34 billion (approx. €50 billion) were signed between 1999 and 2004. A number of big ticket schemes are being procured such as the widening of the M25 (circa £2.0 billion/ €3 billion), Ministry of Defence Military Accommodation (circa £2.5 billion/€4 billion) and a number of large hospitals. But equally significant has been the growing use of PPPs, sometimes on a grouped-together basis, to procure smaller facilities such as the Building Schools for the Future programme with an estimated capital investment of £2.2 billion (€3.25 billion) to be shared between the first 2005-06 wave of 180 schools and the National Health Service’s Local Improvement Finance Trusts programme, with about 51 projects, of which approximately 36 projects have closed. There are a large number of operational facilities that have been delivered using the PFI structure. However in spite of this considerable activity, PPPs represent a relatively small proportion of public sector investment in public services. The UK Government has introduced a number of reforms to enhance the transparency of PPPs and PFIs and accountability, including publishing estimates of future payments for each PPP/PFI and publishing the capital value of contracts signed to date and in the process of being procured. Much of the information on PPPs/PFIs is available through the HM Treasury website, including an online database of projects. In order to improve further the transparency of future deal flows, departments will, from the 2007 Comprehensive Spending Review, publish all Stage 1 value for money assessments that are undertaken in order to determine their likely PFI spend on programmes. The UK Department of Health’s approach to contract summaries is based on a template that specifies the information that should be provided, including:

Other UK Departments are being encouraged to operate under the same guidelines as the Department of Health so that:

The UK PAC committee members can ask witnesses to attend a session if the National Audit Office does not provide the information sought. We were told that they have not tended to have had a major problem with private partners withholding requested information, at least at the operating company level. Indeed the UK business community has been reported as not being opposed to information about contracts being available to the public on the web. However, it was also alleged that PFI projects were the only game in town. If departments did not follow this route then projects were unlikely to receive funding. Thus there was a clear need for a public interest test. As we have seen above, the UK is in an advanced position with respect to PFIs in all sectors of the economy, involving a substantial number of closed projects, with the majority of them in operation. This gives rise to a different set of problems, among them the issue of refinancing and of the possibility of massive financial gains for the private partner. The PAC took evidence on this issue in recent months. 3.2 AustraliaPPPs in Australia have been used to deliver economic infrastructure such as toll-roads, with the private sector taking full market risk, and social infrastructure such as hospitals, prisons and schools, which are based principally on payments for availability and Key Performance Indicators. Full adoption of the PPP model varies considerably across jurisdictions. Victoria and New South Wales (NSW) are at the forefront. Queensland, Western Australia and the Northern Territories have each completed one PPP. 3.2.1 VictoriaThe Victorian Public Accounts and Estimates Committee (PAEC) does not have direct access to all the information held by the private sector consortiums. They have conducted a study specifically on the issue on Commercial-in-confidence and the public interest. Some of their key findings included:

In its most recent report, the PAEC made some more concrete proposals with respect to accountability arrangements. Recommendation 11 The Victorian Government should:

Recommendation 12 That:

Recommendation 13 That:

The Executive Officer of the Victorian PAEC indicated the following:

3.2.2 New South WalesThe Public Accounts Committee of New South Wales does not have an ongoing role in scrutinising particular PPP projects. However, the Committee has conducted a number of inquiries into PPPs over the years, most recently in June 2006. The issue of public availability of information about the private elements of contracts was an issue during this inquiry and the Committee recommended increasing the level of disclosure of information to the public. The Committee expressed the view that contracts should eventually be disclosed in their entirety, which would allow ongoing assessment of a Project and reassurance to the community that the public interest is being maintained. The Committee stated that it is able to call for papers, people and things under the Standing Orders and it has used these powers in the past to require people to produce information. While it does not routinely use these powers to seek particular information about PPP projects, in 2005, when the Committee investigated the comparative value for money from publicly and privately operated correctional centres, the private operator of a centre voluntarily provided complete information to the Committee on a confidential basis. The reports of these inquiries and the government responses can be found on the Committee's website: http://www.parliament.nsw.gov.au/publicaccounts The NSW Government's guidelines for the publication of information about PPPs (called Privately Financed Projects there) were updated as a result of the Committee's 2006 report. The Parliament of New South Wales is bicameral. The upper house, the Legislative Council, frequently calls for the Government to table papers about confidential matters such as contracts for major PPPs. These are often only available for inspection by members of that house. All PFPs are subject to Ministerial Memorandum No.2000-11 and the Freedom of Information Amendment (Open Government—Disclosure of Contracts) Bill 2006, as amended from time to time, which sets specific disclosure requirements arising from NSW Government tenders and contracts.

Detailed below are the items to be disclosed for all contracts and for contracts over $5 million Australian. However, as Schedule 3 shows, there is still a considerable list of commercial in confidence information listed.

NOTE: In addition to these guidelines privately funded public infrastructure projects will still need to comply with the disclosure guidelines set out in the Guidelines for Private Sector Participation in the Provision of Public Infrastructure. 3.3 CanadaAfter a lengthy development process, the PPP model is gaining ground in Canada. The provinces of Alberta, Ontario and British Columbia have been the most active supporters of the PPP framework while interest in Quebec is also growing. British Columbia has seen the most activity having successfully closed eight transactions since mid-2004. Activity has been driven by the need to expand social infrastructure within budget constraints. In June 2002, the province established Partnerships British Columbia (PBC), created to provide “public agencies with expert advice and support to explore and, where supported by a sound business case, to implement P3s (PPPs) and other innovative approaches to provide public infrastructure and services”. British ColumbiaThe following arrangements apply in British Columbia where, after the financial close on all PPP projects:

The Victorian PAEC was particularly impressed with the arrangements that apply in British Columbia. It used it as an example of steps taken by a government to improve the transparency and accountability of PPP arrangements and to demonstrate that community interests are being protected. Section 4 Conclusions and RecommendationsWhen compared to the three countries listed in Section 3, Ireland has still a long way to go with respect to public accountability. The experience in these countries is summarised below. United KingdomThe UK government has responded to criticism of its extensive PFI programme by enhancing transparency and accountability. The UK Public Accounts Committee can ask witnesses to attend sessions if the National Audit Office does not provide the information sought. AustraliaThe Victorian Public Accounts and Estimates Committee (PAEC) has been very active in pursuing the right to access PPP information over the years. The Victorian government puts PPP contracts onto its website after they have been signed, even though this can still take longer than the recommended three month period. In addition the PAEC can ask questions about PPP arrangements during estimate hearings. They are trying to overcome the commercial in confidence clause by directly negotiating with the private partner on wording that might be mutually acceptable. They can also take evidence in private about commercial in confidence matters, but are unable to release that information or documentation even though it might be in the public interest. In New South Wales all PFPs (Privately Funded Projects) are subject to the Freedom of Information amendment Bill 2006 which sets detailed disclosure standards. In addition, the New South Wales Public Accounts Committee is able to call for papers and people and has used this power in the past to attain information about PFPs. CanadaIn British Columbia, detailed project information is placed on the web after close of contract. The Auditor General reviews the value for money disclosure report. Evaluation details are also published. The Committee has taken some account of international experiences in formulating its recommendations. Recommendations

The ever increasing reliance on PPPs for the provision of infrastructure in Ireland as evidenced by the recent National Development Plan 2007 to 2012 indicates that this is an area of growing importance for the PAC.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Analysis of the rationale for the PPP allocation in the various parts of the latest NDP

Analysis of the rationale for the PPP allocation in the various parts of the latest NDP