|

|

|

|

Tithe an Oireachtais An Comhchoiste um Chumarsáid, Muir agus Acmhainní Nádúrtha An Dara Tuarascáil Bonneagar ardluais leathanbhanda náisiúnta a sholáthar [lena n-áirítear na costais ar úsáideoirí agus an cumas chun feidhmeanna Rialtais, Gnó agus Tráchtála a sholáthar tríd an mbonneagar ardluais leathanbhanda náisiúnta] Imleabhar 2 Márta 2004 Houses of the Oireachtas Joint Committee on Communications, Marine and Natural Resources Second Report Provision of a national high speed broadband infrastructure [including the costs to users and the potential to deliver Government, Business and Commerce functions through the national high speed broadband infrastructure] Volume 2 March 2004 α CONTENTS Volume 2 List of presentations List of submissions and supplementary information Section 1 Presentation 1 – Independent National Data Centre Presentation 2 – South West Regional Authority Presentation 3 – Leap Broadband Presentation 4 – Telework & e-Training International Presentation 5 – Ireland Offline Presentation 6 – Southern Health Board Presentation 7 – Health Systems Consultants Presentation 8 – National Centre for Technology in Education Presentation 9 – Atlantic Technology Alliance Presentation 10 – Corevalue Presentation 11 – Dublin City Development Board Presentation 12 – Microsoft Presentation 13 – Hewlett-Packard Presentation 14 – Innovator Presentation 15 – Disability Federation of Ireland Presentation 16 – IAWS – AXIA Presentation 17 – Dr. Sarah Skerratt Presentation 18 – ComReg Presentation 19 – Enterprise Ireland Presentation 20 – IBEC - Telecommunications Industry Federation Presentation 21 – Esat Presentation 22 – Eircom Presentation 23 – Cable providers – NTL Presentation 24 – Cable providers – Chorus Presentation 25 – Mobile Phone operators – Meteor, Vodafone, O2 Presentation 26 – ESB Presentation 27 – MCI Presentation 28 – Global Crossing Presentation 29 – Telecommunications Users Group - IBEC Presentation 30 – C2K, Northern Ireland Presentation 31 – Professor William H. Melody, Economist Presentation 32 – Forfás Presentation 33 – Irish Broadband Presentation 34 – Digiweb Presentation 35 – Meteor Section 2 Submission 1 – AXIA-IWAS Submission 2 – Department of Communications, Marine & Natural Resources Submission 3 – Information Society Policy Unit, Department of the Taoiseach Submission 4 – Digiweb Submission 5 – Eircom Submission 6 – Grant County P.U.D., Washington Submission 7 – IBM Submission 8 – Mediasatellite Ireland Submission 9 – Sky Pilot Submission 10 – Department of Education and Science Presentations by Date

Submissions and Supplementary InformationAXIA-IWAS - Supporting evidence for the Axia Ireland Broadband Proposition Department of Communications, Marine & Natural Resources - Cost of PCs in Schools, figures supplied by NCTE and Datanet Information Society Policy Unit, Department of the Taoiseach - Briefing by the Information Society Policy Unit Digiweb - Broadband Pilot Schemes Eircom - Update on Broadband & Investment Grant County P.U.D., Washington - Presentation to the delegation visiting Ephrata Washington State, U.S.A. IBM - The IBM in Ireland Submission to the National Plan for Women (2001-2005) Mediasatellite Ireland - B-DSL Technical Information Sky Pilot - Wireless Mesh Broadband Network Information Department of Education and Science - Briefing note for members on ICT in the Education Sector PRESENTATION 1 Presentation by Independent National Data Centre PRESENTATION 2 Presentation by South West Regional Authority PRESENTATION 3 Presentation by Leap Broadband PRESENTATION 4 Presentation by e-Training International PRESENTATION 5 Presentation by Ireland Offline PRESENTATION 6 Presentation by Southern Health Board PRESENTATION 7 Presentation by Health Systems Consultants PRESENTATION 8 Presentation by National Centre for Technology in Education PRESENTATION 9 Presentation by Atlantic Technology Alliance PRESENTATION 10 Presentation by Corevalue PRESENTATION 11 Presentation by the Dublin City Development Board PRESENTATION 12 Presentation by Microsoft PRESENTATION 13 Presentation by Hewlett-Packard PRESENTATION 14 Presentation by Innovator PRESENTATION 15 Presentation by the Disability Federation of Ireland PRESENTATION 16 Presentation by Iaws – Axia PRESENTATION 17 Presentation by Dr. Sarah Skerratt PRESENTATION 18 Presentation by ComReg PRESENTATION 19 Presentation by Enterprise Ireland PRESENTATION 20 Presentation by IBEC - Telecommunications Industry Federation PRESENTATION 21 Presentation by Esat PRESENTATION 22 Presentation by Eircom PRESENTATION 23 Presentation by NTL PRESENTATION 24 Presentation by Chorus PRESENTATION 25 Presentation by Mobile Phone Operators PRESENTATION 26 Presentation by ESB PRESENTATION 27 Presentation by MCI PRESENTATION 28 Presentation by Global Crossing PRESENTATION 29 Presentation by Telecommunications Users Group - IBEC PRESENTATION 30 Presentation by C2K, Northern Ireland PRESENTATION 31 Presentation by Professor William H. Melody, Economist PRESENTATION 32 Presentation by Forfás PRESENTATION 33 Presentation by Irish Broadband PRESENTATION 34 Presentation by Digiweb PRESENTATION 35 Presentation by Meteor Broadband for IrelandHEARTWATCH and the Independent National Data Centre Dept. of Communications, Marine and Natural Resources -Mr. R. Lenihan -Mr. F Marrinan T. Cahill, Independent National Data Centre Tom Cahill (marlow data services)

– Broadband & telecoms / internet – 10 EU country offices / >80 monitoring sites – WAN -Dublin Operations centre – Emerging Internet (dial up) for customers – EDI, CRM and SCM in Nortel Networks – Spar, An Post Intranet in PostGEM / IOL – Eircom and Eircom.net (Transformation) – Europe’s largest hosting & colocation company – High-end broadband users – Carrier neutrality (AT&T, Bell Canada (Teleglobe), BT (ESAT), C&W, Colt, Eircom, KPN Qwest (Ebone), Irish Broadband, Packet Xchange etc) – IBM Premier partner, Oracle & SUN certified HEARTWATCH

HEARTWATCH Targets

INDC / ICT and the ‘Ideal’

ICT – How it is….

INDC dependencies

INDC: Operating Environment

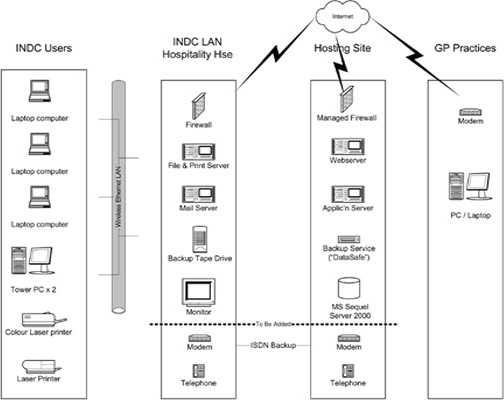

INDC - Service Providers

– Security (physical & logical (Managed Firewall)) – Backup (“Datasafe”) – Basic Support – Basic Monitoring (ports & URLs) – Performance Monitoring (not required) – Internet (not much needed here) – Server (set up & development) – Interim tool (set up, development & trouble-shooting) – Support (server application) – Web applications (not required) – Support INDC

– Integration with existing PMS (these are GPs after all…) – Changes in Clinical Data Set and PMS Vendor reaction – Adjustments / upgrades to applications – Trial studies / ad-hoc investigations – Integration with other databases Broadband & GP Practices

– ‘Always on’… (must have security, backup) – (Possible ‘dot.net’ implications…) – Firewall and router (€200 – 700) – User skills – H/w and OS investments… PMS Vendors

– Minimum standard ‘Integrated PMS’ with data import functionality – ‘Seamless’ interface with web-based applications – Probable long-term transition to ASP model, leaving database stuff to INDC-like operations INDC -ImplicationsHosting & Telecoms… – Security (physical & logical (Managed Firewall)) – Backup (“Datasafe”) – Basic Support – Basic Monitoring (ports & URLs) – Performance Monitoring (applications & database) – Internet (more of this!)

– Server (set up & development) – Interim tool (set up, development & trouble-shooting) – Support (server application) – Web applications – Support INDC – web-based App

Possible future scenarios

Questions

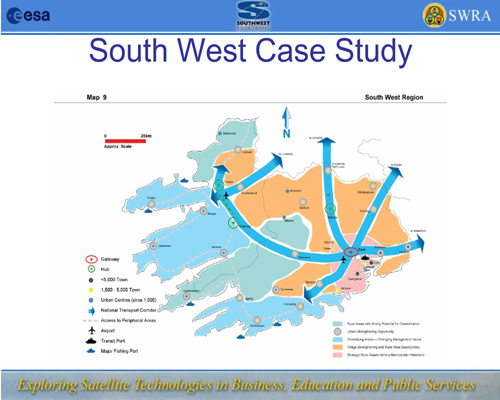

Presentation to the Oireachtas Joint Committee on Communications, Marine and Natural Resources June 4th, 2003 John McAleer Director South West Regional Authority Information and Communications Technologies Potential benefits include: » Death of distance » Overcome peripherality » New methods of working » Access to markets Ireland’s Knowledge based economyIncreasingly Ireland’s economic output is based on knowledge rather than raw materials ThereforeAccess to ICTS is increasingly important to the sustainability of all areas of the State Broadband dependency

Regional Authority Strategic Objective

All of these objectives are challenged by lack of bandwidth Throughout Europe

The Case for Satellite Broadband

European Space Agency

The use of Satellite technology to deliver broadband to regions throughout Europe South West Broadband project

Conclusions and recommendation

and As the systems are fully scalable, priority bandwidth could be ascribed to particular users when required. Cost effectiveness

Taking the matter forward

Go raibh maith agaibh John McAleer Director South West Regional Authority jmcaleer@swra.ie Project Website – www.swra.ie/broadband.

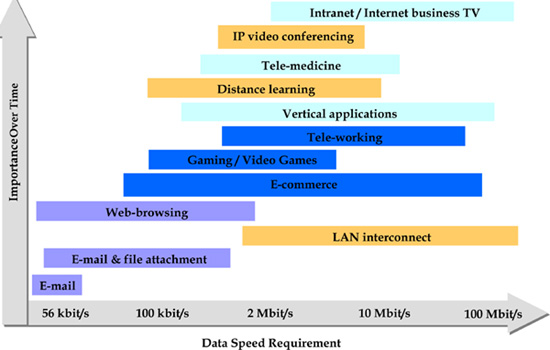

leap broadbandIreland’s Number 1 for Business Broadband Rory Ardagh Introducing Leap BroadbandLeap Broadband is the most successful ‘new entrant’ Broadband operator in Ireland with a, large, growing and Broadband enabled customer base Leap Broadband is a specialist Broadband Internet Provider, and aims to be Ireland’s premier provider of flat rate, always-on Internet access and data services to the business community Leap Broadband is Dublin based, and Irish owned. Founded by brothers Rory & Charlie Ardagh and Bart Bonsall to develop a network which will provide faster access to the Internet at more affordable prices than previously available on the Irish market. Applications driving broadband demand

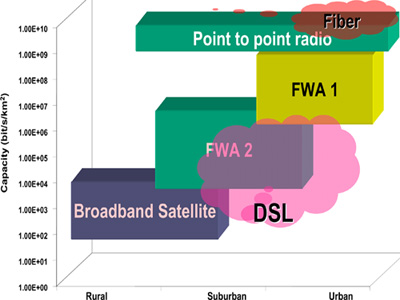

internet access today Broadband Technology Comparison

Cable Modems Omitted:

Fiber

Point to Point Radio

FWA 1

FWA 2

DSL

Broadband Satellite

FAST -the Leap Broadband AdvantageFlat rate - our highly competitive pricing enables businesses to spend as much time online as they wish without having to consider per minute call charges Always-on connections to the Internet - no dialing in to check, send or receive emails or browse the Web Scalable – Leap Broadband is a flexible service giving you bandwidth on demand so your Internet requirements grow with your business Timely - the business critical benefits of Leap Broadband Internet access and data services can be installed within days

Some Leap Broadband Customers

3 Main Issues Facing Leap“All consumers … deserve a new spectrum policy paradigm that is rooted in modern-day technologies and markets. We are living in a world where demand for spectrum is driven by an explosion of wireless technology and the ever-increasing popularity of wireless services. Nevertheless, we are still living under a spectrum ’management’ regime that is 90 years old. It needs a hard look, and in my opinion, a new direction.” Chairman Michael K. Powell, Federal Communications Commission, October 30, 2002.

3 Main Issues Facing Leap

3 Main Issues Facing Leap

leap broadbandIreland’s Number 1 for Business Broadband Rory Ardagh E-Training InternationalPresentation to the ICT Sub-Committee of the Joint Committee on Communications, Marine and Natural Resources Nana Luke Director, E-Training International Chairperson, Telework Ireland Overview

The question is no longer Why do we need broadband? The question is: How quickly can we roll it out? Fast -tracking WANs for rural areas is the way forward. Broadband is essential infrastructure - this is not a regional or market issue. Who we are

– Martina Minogue – Nana Luke – East Clare Telecottage (est. 1991) – Taylor Lightfoot Transport Consultants (est. 1990) Location -Rural: – Office premises in Main Street, Scariff, Co. Clare and home offices – Rural Market Town in East Clare, 25 miles Limerick, 22 miles Ennis. – Population 900, including hinterland 1,500 – Comms: ISDN & PSTN Chances of getting broadband through market forces – not good! What we do

– OASIS, BASIS, REACH – Roche, IBM, Trumpf – Dept. of Justice, Equality and Law Reform, NDP Gender Equality Unit – Rural Resource Development (Clare LEADER) - Evaluation of IT resources in Co. Clare – Clare LES – FÁS Shannon – FÁS Curriculum Development Unit – Intuition Publishing – Primelearning.com – 4th and 5th FP – Leonardo da Vinci – ADAPT – eContent How we do it

– All World Languages – Many specialist areas of expertise – instructional design – technical writing – graphic design – webdesign – programming – administration – surveys & data entry Benefits of eWork ModelPersonal benefits: – Work where you live – Very short commute Business benefits: – Flexibility: Core staff in small premises, project based eTeams work from home offices – No skills shortages! Knowledge Based Business

ideal for more rural areas Benefits to community & for regional development

– ICT equipment – training – services Our need for broadbandKnowledge based business - Needs: – Always online – Affordable Flat Fee Access – High speed connectivity

Has to survive on: – Frequent dial-up via ISDN – Expensive metered access – Slow connection speeds

Scariff Community Broadband ProjectCommunity Broadband Project – Source Broadband Access to the Internet – Make available to Local Community via WAN – Leverage high speed Internet Access & even higher speed Local Area Network for:

Submitted to: – Dept of Communications, Marine & Natural Resources – Dept of Community, Rural and Gaeltacht Affairs (CLÁR) Interested Participants: – Scariff National School – Scariff Community College – Scariff Medical Centre – Derg Credit Union – Bank of Ireland – Scariff Library – Local Businesses – Local Sports Clubs – Local Development Groups – Clare County Council – Shannon Development CLÁR Area: – Flagmount National School – Killanena National School – Home based eWorkers The need for broadband

– Equal access for schools & children at home – Business competitiveness Cost & speed of broadband access – New Business opportunities! – Access global Markets from anywhere! - If we don’t, others will! – Much cheaper, faster, more interesting Internet Access. – Rural location must not be a barrier! – 33% poductivity gains on top of 20% for dial-up eworkers! – Balanced regional development Evaluation of IT resources in Co. Clare

International Comparisons

By 2008:

– Available to 47.4% of homes – 55.9 % of schools covered – 50.6% of Libraries covered – Pilots for rural access in progress Urgent Action required!

Why do we need broadband? How quickly can we roll it out? Essential in order to stay competitive!

It is now easier to get broadband in Botswana and Romania than in Ireland! (52nd out of 81 countries) – Suitable Internet Access – Distribution of Infrastructure – Maintenance of Infrastructure not adequately planned or funded (28th) ..especially in rural areas

– broadband access should not be dependent on location /regional activities Useful linkseWorking and Teleworking

Alternative Irish Broadband Coverage www.eircomtribunal.com

International

EU Objective One, BT, SW Regional Development Agency, Enterprise Agencies, Cornwall College BT’s site to stimulate broadband uptake – transparency, trigger levels General Internet

Has taken over Nua. Global Internet Stats. Irish & International Tech News mail: chairman@IrelandOffline.org www: www.IrelandOffline.org

Broadband - The Next Steps for Ireland Ireland Offline 4th June 2003 Contents

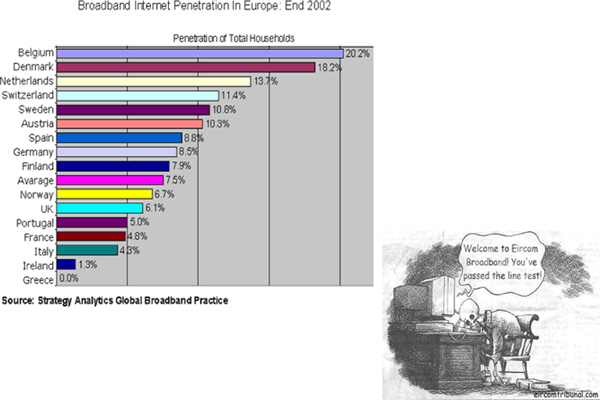

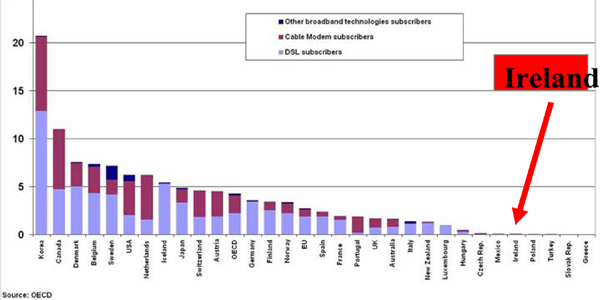

1 Introduction1.1 About Ireland OfflineIreland Offline was formed on 13 May 2001 in response to the closure of an off-peak flat rate ISP service earlier that year. Since then it has evolved into a campaign group highlighting deficits in flat rate dial-up Internet access and broadband. Ireland Offline has been successful in lobbying for flat rate and such services are due to be introduced towards the end of June, 2003. Ireland Offline is an independent organisation and has no affiliations with any commercial organisations. In this document we make a simple argument. Ireland is behind in the development of broadband technologies due to the lack of appropriate supply (not demand). This lack of supply is due to lack of competition particularly at the last mile infrastructure level. To solve the problem, competition in the form of alternative last mile infrastructure needs to be introduced. 1.2 The term “broadband”.In recent years, the term “broadband” as it is commonly used internationally has come to mean the sort of high speed Internet access typically available through cable modems and DSL (digital subscriber lines) at a price affordable by homes and small businesses. Speeds offered by these means are usually a multiple (ten to fifty times) of that offered by analogue modems over telephone lines. The common usage usually does not include corporate digital communications via, for example, leased lines. In Ireland, “broadband” sometimes refers to the regional fibre infrastructure, however in this document, the term will refer to those services as defined by the common international usage of the term as outlined above. In addition we would not class wireless LAN “hotspots” as broadband since these do not provide residential or small business access. Hotspots are an example of what can be achieved for a couple of hundred euros once broadband is available at a particular location. They are not a solution to the problem of providing broadband. 2 Market overview2.1 International viewsA number of International reports have highlighted Ireland’s poor performance in introducing broadband. In October 2001, the OECD [OECD 2001] ranked Ireland 27th out of 30 OECD countries in the development of broadband access. In February 2003, the World Economic Forum placed Ireland 51st behind Namibia, Peru, Nicaragua, Botswana, Dominican Republic, Mexico, Guatemala, Brazil and Romania [WEF 2002]. In fact Ireland is lower than half way down on a list of 82 countries that includes some of the poorest in the world. In May, 2003, the Swiss Business School, IMD, ranked Ireland last of 29 small economies for “Suitable Internet Access (availability, speed, cost)” in their World Competitiveness Index.[IMD 2003] 2.2 The demand for broadband.In 2002, ComReg commissioned a report from the market research company, MRBI, [MRBI 2002] to find out the level of demand for broadband. Without the issue of price mentioned, they found that 46% of respondents (sample of adult population) were likely (32% fairly likely and 14% very likely) to get broadband if it were offered. They also found a large degree of price-sensitivity in the demand for broadband. There was approximately five times the demand at EUR 30 than at EUR 60 with negligible demand at EUR 70 or above. At the time of the survey, the only broadband that was available to most people was DSL in the region of EUR 100 and above. In the Irish market, there is significant demand once the price approaches European averages in the region of EUR 30 to EUR 40. If this demand was met, Ireland would lead Europe in broadband take up. 2.3 Current Irish broadband market2.3.1 Broadband Penetration (% of population) [ECTA 2003].

The above table shows that Ireland is currently second from the bottom in a table of EU countries for broadband per head of population. Belgium has over 48 times the broadband penetration of Ireland. 2.3.2 Growth in broadband (per 1000 population)[ECTA 2002] (from end of June 2002 to end of March 2003).

This table shows that not only is Ireland second from the bottom for broadband penetration, but when compared with the figures for end of June 2002, Ireland is also growing its broadband connections much more slowly than other countries. Ireland continues to fall farther and farther behind at an alarming rate despite modest developments. 2.3.3 Explanation of Ireland’s poor broadband performance:- Lack of infrastructure competition.The low broadband penetration and low growth in that penetration can be explained easily. Apart from cable modem Internet (covering at most 40,000 homes in Ireland) the vast majority of consumers in the country either had no access to broadband or, where available, broadband based on telephone lines and services was provided by the incumbent telephone company and resellers. Until recently, DSL provided by both Eircom or one of its competitors operating under LLU (Local Loop Unbundling) regulations, was only available in limited areas and the entry-level services were priced at over EUR 100, well above the international norm (EUR 30 -50) and outside the range considered affordable by residential customers. Also, the number of exchanges that were enabled to provide DSL was low and the line failure rate appeared to be high with one user group reporting an 80% failure rate. We believe that this was due to poor quality of lines and “pair gain” systems (devices which allow two virtual lines to operate over a single copper pair). The reason for the high price is a lack of competition. 2.4 Historical background.In other countries, cable TV companies have led the way in providing residential broadband. Broadband Internet via DSL was developed initially in the US in the mid- 90s as a means of combating competition from cable companies undermining revenue from dial-up Internet. It is unlikely it would have been offered otherwise. Ireland has very high cable TV penetration, however very little of this is of a standard which supports two-way communication. Historically, cable TV became popular in the late ’60s and early ’70s during a time when only one Irish terrestrial TV channel was available and the public was willing to pay for more choice. What was known as “communal aerials” were erected so that a large central antenna could be used to receive British terrestrial channels. The signal was then relayed to homes via coaxial cable. These local systems were subsequently amalgamated into larger cable TV companies. Because the original appeal of cable TV in Ireland was to provide an access to a few additional channels, the capacity of the systems remained low. In other countries where multiple terrestrial channels were already available, cable TV developed along different lines. Consumers already had a choice and therefore the cable TV providers had to provide a multitude of extra specialist channels like film and sport in order to make the package attractive. In addition, because the cable networks were developed later, the cable companies were not burdened with legacy infrastructure. Belgium, for example, has the highest broadband take up in Europe and also has very significant competition from cable TV with 41% [ECTA 2003] opting for cable modem Internet access. 2.5 Recent developmentsFrom a high of EUR 107 for basic broadband, the price has come down to between EUR 50 and EUR 56. This has been made possible by the addition of a new bitstream1 service at EUR 27. While still expensive by European standards (norm: EUR 30 to EUR 40), we expect take up to increase somewhat. Unfortunately, prices are unlikely to come down further due to the still high (by European standards) bitstream wholesale rate of EUR 27. Excluding Ireland, bitstream ranges from EUR 13.3 in Belgium to EUR 25.4 in Austria [Infosoc 2001], making Ireland’s bitstream DSL the most expensive in Europe. We believe that this reduction is largely due to the immanent introduction of flat rate Internet packages at the end of June 2003 as predicted in the Analysis Consulting report for Forfás [Forfás 2002]. There are plans for 150 exchanges to be enabled by September 2004 but no plans for the remaining 950 exchanges. These exchanges are outside large urban areas. In addition, there has been an increase in competition from wireless operators in the Dublin area. Two companies now operate from Three Rock Mountain offering residential broadband in the EUR 50 region. One of them is trialing a EUR 30 service in the Tallaght area of Dublin. Also, the companies Net1 and Digiweb have begun offering wireless services in Louth, and Amocom in Cork. Apart from these welcome exceptions we remain in the situation where one company controls most of of the market - several others reselling aspects of this. The illusion of competition is maintained by the requirement of this company to provide appropriate wholesale services for each of its retail services. Although this allows competitor companies to make money, the actual services provided depend on innovation by the incumbent telephone company. ComReg’s MRBI demand survey shows that calling for demand-side initiatives is a smokescreen for inaction and high cost. Ireland has as much demand for broadband as other countries (see 2.2, The Demand for Broadband). 3 Current attempts to solve the problem.3.1 Metropolitan area networks.This solves the problem at a local but not last-mile level, however it will be essential for providing cheap backhaul for wireless broadband operators. Unfortunately, current plans seem to be slipping. The original plan outlined on 7 March 2002 was that 123 towns with populations over 1,500 would be completed. 67 towns would be provided with fibre rings by the end of 2003. However more recent announcements seem to indicate that only 19 of them will be completed by this year. This casts doubt whether the full project will be completed in five years. 3.2 Government-funded wireless projects.

In addition to this, through EU funding, the BMW assembly has provided grants totaling EUR 250,000 for wireless projects providing broadband in Ballinlough Co. Roscommon & Ballyhaunis Co. Mayo, Strokestown, Co. Roscommon and Virginia, Co. Cavan. 4 What needs to be done.Taking into account the lack of last mile competition and consequent lack of innovation, the solution will require developing alternative last mile solutions. 4.1 Looking at alternatives:1. Wireless: no ultimate bandwidth limitation. No single ownership of the broadcast medium - individual operators hold or share spectrum allocations. Plenty of empty spectrum for future development. Downside - line of sight problems to some locations with particular technologies and frequencies. 2. Upgrading the cable system - very expensive - still have bandwidth limitations. Ownership of infrastructure limited to one company. 3. Powerline broadband. More bandwidth possible. Will ultimately hit limitations based on capacity of signal over copper. Another case of one company owning the last mile infrastructure hampering innovation. 4. FTTH (Fibre optic To The Home) - no upper limit to bandwidth. Very expensive. Ownership in the hands of one entity - there would have to be controls over coverage and pricing -vendor neutral wholesale. 4.2 Conclusion: prioritise wireless.In our opinion, it is no longer time for trials. Immediate action is necessary and a proven alternative last mile technology exists. If one of these solutions were to be pursued exclusively, we believe it should be wireless because it provides the most scope for competition and innovation. Not only between wireless providers and ’wired’ providers but also between wireless providers themselves. Wireless is not one single technology (like broadband over powerlines), but a family of technologies. Wireless is currently the focus of major technological innovation for the delivery of broadband over the last mile in terms of range, bandwidth and cost. If the Government was to commit itself to the rollout of a nationwide competing wireless infrastructure, we stand to position ourselves to benefit directly from this innovation. We believe that by pursuing this strategy, Ireland would become not only the equal, but better than its peers for availability, cost and speed of Internet access. This is because, with a national wireless infrastructure in place, the continued technological innovation in wireless will have an immediate impact on innovation in services and, as a consequence, the other providers of broadband have to continually innovate to compete, something which will not happen in countries where cable is the competing broadband medium. 5 Recommendations.5.1 Support and fund local initiatives.Up to a fifth of households in Ireland that are not connected to a public water supply are served by Group Water Schemes, with subsidies provided for infrastructure and training. In a similar manner, local co-operatives should be supported for the provision of local connectivity needs, DublinWan being an example of such a community group. As well as funding for community initiatives, there should be increased funding for commercial initiatives particularly outside of large conurbations. In this respect, Government funding for Digiweb and Amocom is to be praised and encouraged. However, significantly more in this regard needs to be done. 5.2 Increase availability of affordable backhaul.Facilitate affordable, simple connection to backhaul: The Government’s Metropolitan Area Network should be accelerated to reach its original target of 123 towns by 2007. ESB should be instructed to increase the number of POPs (points of presence) for connecting to backhaul and also sell capacity in smaller chunks. Currently the minimum available is 155 mbits/second, whereas chunks of 2mbits/second are more reasonable for local service providers and communities. 5.3 Raise public awareness of alternative technologiesA public awareness campaign highlighting alternative platforms for broadband delivery. This will help combat any consumer ’inertia’ that may be present with regard to switching from established platforms. Consumers should be made aware that DSL and cable modems aren’t the only possible means of getting broadband. Although there are no known health issues with wireless broadband, consumers may be wary of adopting such technologies. References[ECTA 2003] ECTA April 2003 (cable + DSL figures). http://www.ectaportal.com/ectauploads/dsl_apr03.html [CIA 2002] CIA World Factbook http://www.cia.gov/cia/publications/factbook/ [ECTA 2002] ECTA June 2003 (cable + DSL figures) http://www.ectaportal.com/regulatory/dsl_jun02.xlshttp://www.ectaportal.com/r egulatory/dsl_jun02.xls [Infosoc 2001] EU Information Society, 8th Implementation Report. http: //europa.eu.int/information_society/topics/telecoms/implementation/annual_report/8threport/finalreport/com2002_0695en01.pdf [Forfás 2002]Forfás: Broadband Investment in Ireland. Review of Progress and Key Policy Requirements. http://www.forfas.ie/publications/ bband02.htm [OECD 2001]OECD - The Development of Broadband Access in OECD Countries, October 2001. http://www.oecd.org/pdf/M00020000/M00020255.pdf [IMD 2003] IMD - World Competitiveness Index. http://www02.imd.ch/wcy/countrylist/ [WEF 2002] World Economic Forum - Global Information Technology [MRBI 2002] Consumer Demand for Broadband in Ireland - Findings of Survey Ian McShane, Managing Director, MRBI. http://www.comreg.ie/_fileupload/publications/IanMcShane.pdf

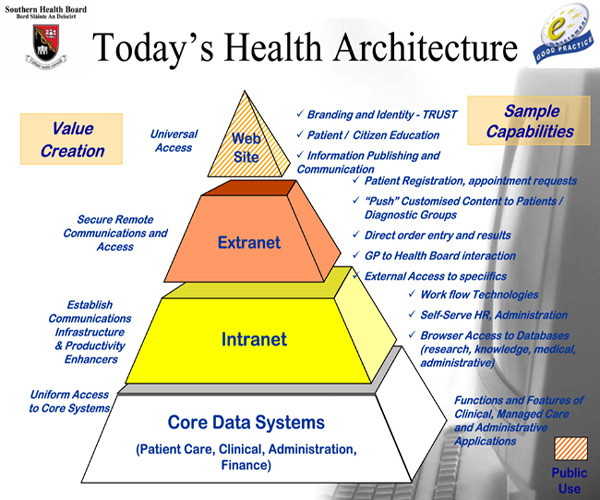

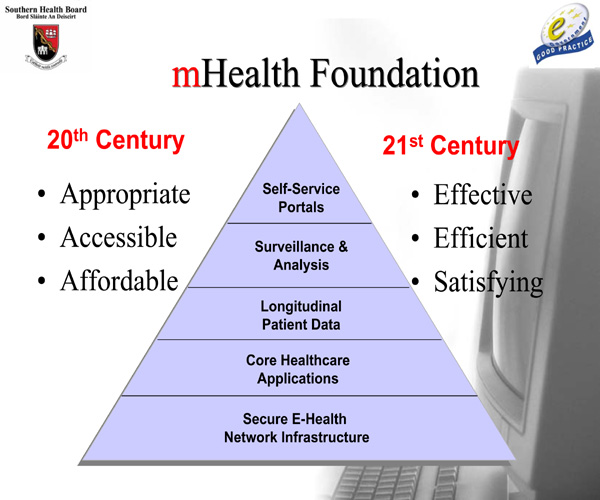

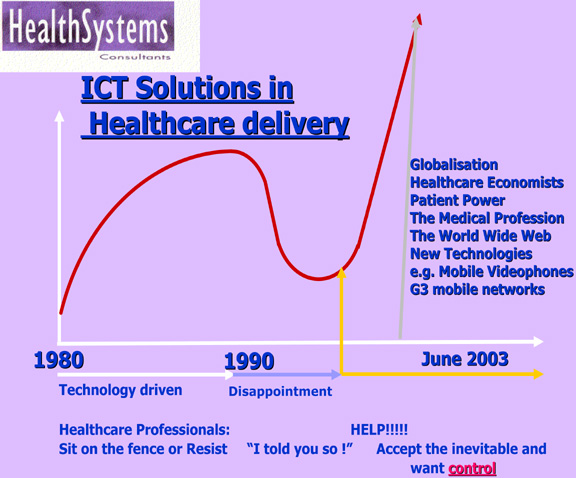

mHealth If you don’t know where you are going…. any road will get you there? Even though there are a lot of possibilities it’s still important to set a direction. eGovernment is providing direction and opportunities so we need to introduce new technologies with business / service models in a way that maximises potential.

mHealth Government + Health

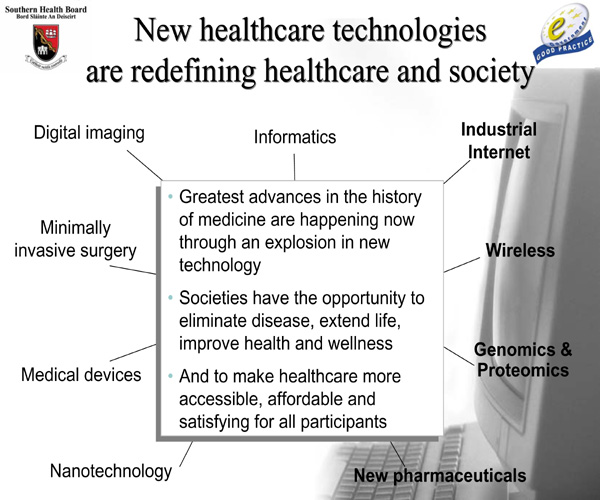

……There is structure in HealthcareFoundation Technologies

Advanced Technologies

– Cost control – Information access – Clinicians, Healthcare Professionals – Patients, Citizens 1.We need to understand that large advances are coming within 3-5 years, and current investments may require replacement / upgrading 2.Develop strong healthcare professionals education programme today to prepare for the tools that will be available in the near-and mid-term A short overview of the SHB experiences addressing the challenges and opportunities of eGovernment Health eSHBEnvironment

10 Goals 1. Integration of patient based services 2. New ways of delivering services and information 3. Manage information as an asset 4. Manage creation of knowledge 5. Optomise use of resources 6. Create an effective organisation 7. Achieve an Electronic Health Record [EHR] 8. eEnable Clinical Systems 9. eEnable Administrative Systems 10. Develop an enabling Technology Architecture What do we mean by that?

– Listening Days, eGovt Initiatives, – Medical Protocols, Research, Best Practice

Practical Examples

– Births, Death & Marriages – Environmental Health, Bridges Dental – Community, Mobile Computing Interactive Hospital School

MOBILE … COMMUNITY PIMs

Integrated EHR Where are we going now?

‘E’…. is not just about computers and systems. It is about people and processes and most importantly it is about thinking differently…. eSHB….. 2001 Opportunity and ChallengeContact Details:- Ursula O’Sullivan eMail:- osullivanu@shb.ie Web:- www.shb.ie Phone:- 021-4922990 eHealth eEurope eVolution Dr Ricky J Richardson BSc MBBS MRCP(UK) FRCP FRCPCH DCH DTM…H Chairman - UK eHealth Association Chairman – Pan European eHealth Working Group Pan European eHealth Working Group European Health Telematics Association - EHTEL Clinical Director – HealthSystems Consultants Ltd Consultant Paediatrician Great Ormond Street Hospital for Children, London The Portland Hospital for Women & Children, London The Speech, Language and Hearing Centre, London Health is far too important a subject to be left in the hands of the medical professionals !!!! Dr Halfdan Mahler - DG Emeritus - WHO after Oscar Wilde

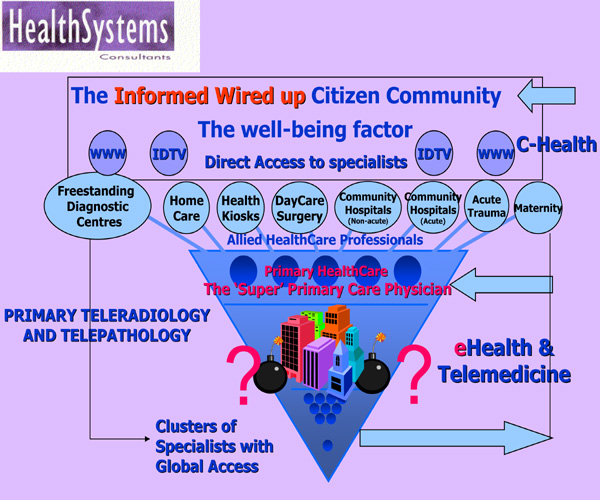

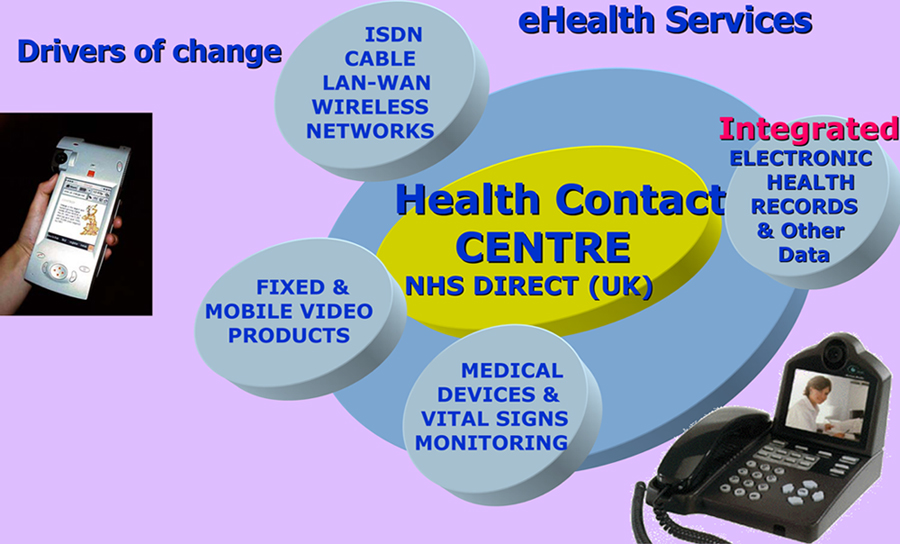

Who will be the primary care physician of the future? The ePatient ! What is eHealth?

eHealth

TeleConsultations (previously Telemedicine) Clinical Decision Making Support Software Vital Signs Monitoring Services TeleHomeCare - National ePrescribing Services - eNursing

The Paradigm ShiftThe Seven Drivers Forcing Change

The Impact of Globalisation on Healthcare deliveryHealthcare Services move into the Retail Environment Shopping Mall medicine C-health: - Health-on-line Websites District General and Regional Hospitals become obsolete as a concept Emergence of Epicenters of Medical Excellence

The Paradigm Shift The ImpactHealthcare Professionals

Patients

The Paradigm Shift Who will be the Primary Care Team of the Future?The Informed ePatient

Will the family doctor become “The Wellness Guardian-Caretaker”?

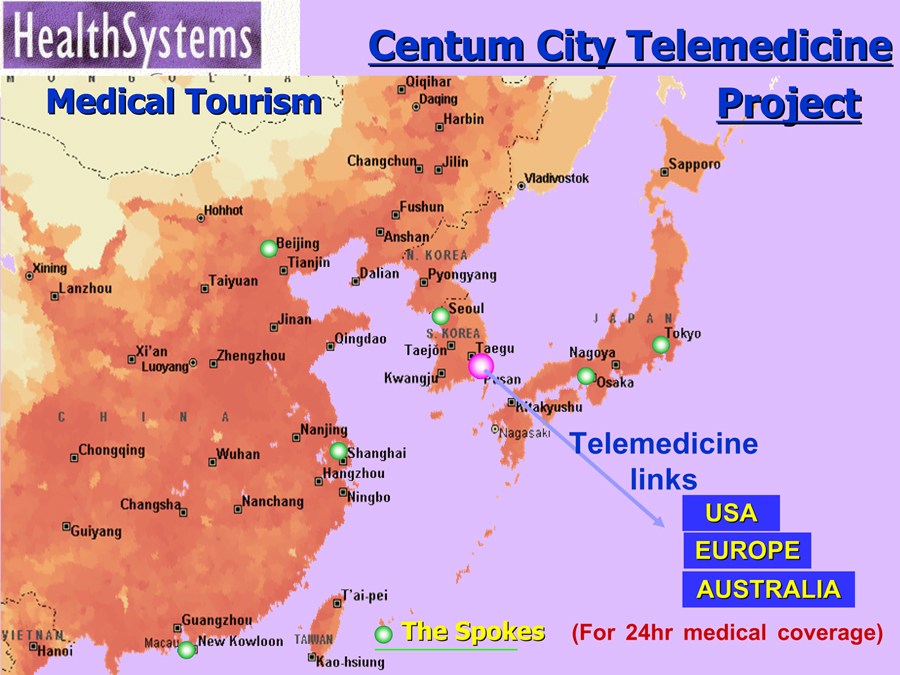

Telemedicine … eHealth The story so far

European CommissionMission Statement To make medical services - wheresoever sourced - ubiquitously available across Europe

European CommissionIssues in Europe Ageing Population Candidate Countries – different levels of care Present Healthcare Models --- Unsustainable Solutions Drive point of care outwards eHealth everywhere Migration of Patients Healthcare Professionals

European Health Telematics AssociationMission

eHealth Working Group (T2/T9) - EHTEL Original Objectives Virtual Demonstration Capability – eHealth Best Practice Website – Launched October 2001 Identify barriers to the widespread Deployment of eHealth – Promotion at all levels Three Physical eHealth Demo sites Nestor/Motion Media Ireland ?????? Third site Position Paper – eHealth for Europe for delivery Feb 2002

eHealth Working Group - EHTEL Original Objectives (continued) Solicit Industry Support – GlaxoSmithKline, Siemens, DTI (UK), Motion Media, PolyCom--Achieved and ONGOING Grow the membership to reflect all member states - ONGOING Invite candidate country representatives as observers – ONGOING Regular Meetings - eHealth Working Group Members four meetings annually Executive - monthly

eHealth Working Group - EHTEL Deliverables – before July 2003 Presentations at leading telemedicine conferences across Europe Achieved and Ongoing Face to face meetings with senior Government Ministers, Civil Servants and Healthcare Professional Bodies across Europe Achieved and Ongoing Publications (peer review) and Media Appearances Achieved and Ongoing Self Certification process for website Achieved and Ongoing Physical eHealth demo sites Achieved and Ongoing Position Papers Months 12 and 30 Month 12 Achieved Month 30 Ongoing

eHealth Europe Where have we reached? The Revolution is OVER ! eHealth is in……………. eVOLUTION! There is much to be done!!! eHealth

- National ePrescribing Services - HomeCare Monitoring - eNursing - eMinistry of Health online websites Urgent Requirement eHealth and the NHS - UK The Consequences National ePrescribing and eBooking Services All Citizens - Electronic Health Record - ICRS Massive use of - Home TeleCare - Vital Signs Monitoring - eNursing Patients have choice of location and healthcare personnel Changing role for - Primary Care Practitioners - Pharmacists - Nurses The Telemedicine Blueprint Malaysia

Four Flagship Applications

Concurrent implementation leads to reform 20 year implementation plan

Capability Through Partnerships “Whatever affects one directly, affects all indirectly” – Martin Luther King

Large scale complex programmes benefit from an Integrated Approach Need to work in Partnership to deliver the best results A Holistic Approach A Systems Approach. Building a Partnership The South African Experience Provide bespoke programmes based on understanding of local and international policy and standards as well as commercial developments.

The Developing World Can leap-frog the traditional evolutionary process

Is this acceptable in our world?

Health Equity for the global community eDissemination of Healthcare Professional education & public health information leads to ePrevention

The Healthcare Team Doctors, Nurses, Pharmacists Technicians Administrators

If you want to work as a team You must train as a team Tan Sri Dato Dr Abu Bakar bin Suleiman May 2001 - Jeddah The eHealthcare Team Doctors, Nurses, Pharmacists, Technicians, Administrators

Integration of Health Sciences is the utmost priority to train the future eHealthcare professionals Train as a Team, Work as a Team Place the Patient at the centre of Care Future eHealth environment

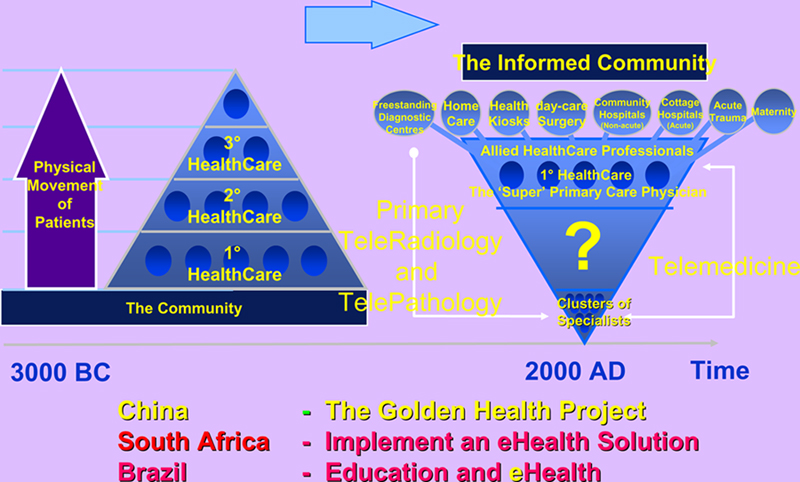

Healthcare Delivery in the new Millennium Where are we going?

- Traditional Medicine} - Preventive Medicine} At Primary care level - Self Treating Patients} “The Wellness Guardian” - Curative Medicine}

eHealth The Major Consequences Improvement of skills at primary care level The InterNet (Broadbandwidth) Constant Physiological Monitoring - Homecare Access to global Epi-centres of medical expertise Integration of medical, health, genomic, environmental, socio-economic data for ePrevention - Global Health Equity

What’s on the electronic health horizon? Welcome to 2010

Call My Agent The personal digital assistant of the future will do a lot more than organize our schedules and plan our days. In an overwhelming sea of data and messages, the Agent will use rudimentary artificial intelligence to sort, store, and forward info and messages based on individual priorities, preferences, and interests. It will interact with the earphone and all digital devices at work and at home, connecting them to the Net and instantly updating them. Think Palm's HotSync times 10. Say goodbye to money, keys, credit cards, beepers, and TV remotes.

Phones will be low-powered, lightweight, ear-mounted, and equipped with one follow-you phone number. It connects to the Net via the Agent PDA.

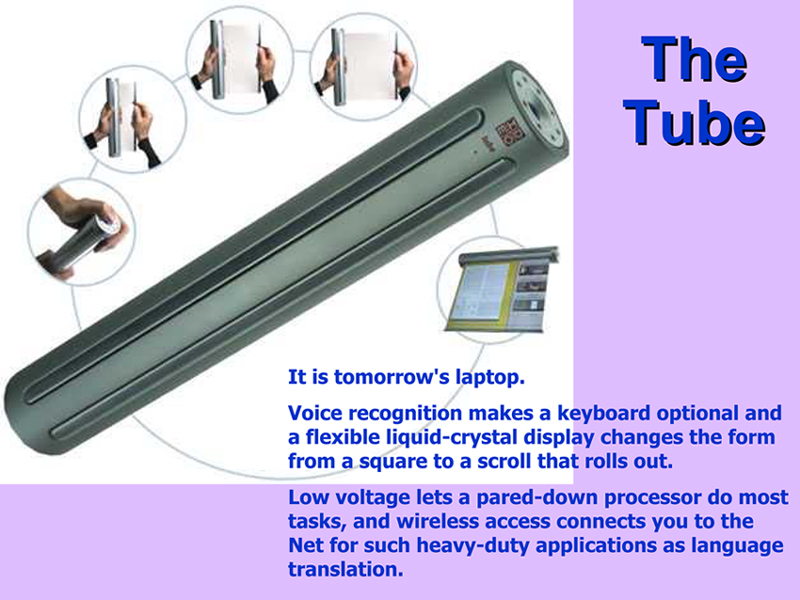

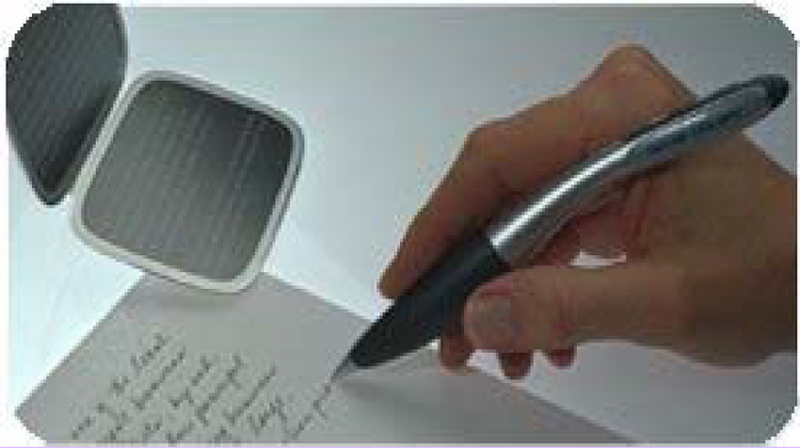

As you write with this pen, it captures your scrawled messages and beams them to your Agent PDA or your Tube rollup monitor.

Electronic ink and GPS combine to provide a lightweight moving map that displays your exact location in all terrains.

Comfort Zone

In a completely wireless world, control over private space will be at a premium. Cell phones will be ringing and screens will be flashing, drowning people in a sea of data. Eyewear can provide a cone of silence and a zone of privacy.

Smart Cubicles Workstations open completely, and the space becomes "alive," with computing and communication technology embedded in furniture and walls. Desks become optional as interactive screens hang from canopies, programmed to do documents, multimedia, spreadsheets, or ambient art. Smart chairs cancel noise and maximize comfort. In one generation these workstations can be controlled by thought?! Medical Mirror

Broadband

Where are the challenges?? Not the technology - The People

Health is far too important a subject to be left in the hands of the medical professionals !!!! Dr Halfdan Mahler - DG Emeritus - WHO after Oscar Wilde eHealth In the new world order, the ePatient will be in an electronic care continuum with global medical knowledge Dr Ron Merrell, Virginia Commonwealth University, USA Prishtina, Kosova, October 2002 The Watershed Generation Gap

Mary Lobascher 2000 Value of Broadband to schoolsCurrent status of ICT in schools NCTE conducted a full national census of ICT in schools on three occasions: in 1998 (with Telecom Eireann), in 2000, and in 2002. The census had an overall response rate of 83%, Some Initial findings of ICT in schools census 2002 Numbers of computers The schools that responded reported a total of 67,350 computers. These figures may be adjusted upwards to take into account the schools that did not respond. Assuming that the schools that did not respond had the same average number of computers as those that did respond, this suggests that the total number of computers in schools was 84,663. This is a 65% increase on the number reported in 2000 (51,307). Number of computers and pupil computer ratio

Since1998, based on an investment of some €140m, significant progress has been made in this regard. Schools were asked to report the amount of money spent on ICT in addition to the grants received from NCTE Additional expenditure on ICT

Pattern of Pupil Computer ratio The 2000 data revealed that disadvantaged schools were better-equipped, on average than other schools. This pattern continued in 2002. Disadvantaged primary schools, on average, had a pupil computer ratio of 10.5 to 1, compared with 11.9 in other schools. At the post primary level the disadvantaged schools had an average of 7.8 students per computer, compared with 10 for other schools. Disadvantaged schools

In 2000 there were significant differences in level of equipment between different types of post primary school. Vocational schools were the best equipped, and voluntary secondary schools were least equipped. These patterns persisted in 2002. Vocational schools had an average of 66. pupils per computer, compared with 8.3 for community schools and 11.3 for voluntary secondary schools. Post primary school type

Location of computers in the school

Classrooms with ICT

Networking and Internet access

In 2000, 69% of post primary schools had Internet access via an ISDN line, but by 2002 this had risen to 85%. While most post-primary schools had ISDN, very few had broadband, with only 3.5% having DSL connections, and 1.9% having satellite connections. In the primary and special schools the picture was and remains very different. The majority of schools were using telephone lines to access the Internet, and less than one third had ISDN connections Internet connection

Use of the Internet

Pupil use of the Internet and email

Type of Internet use

School priorities and needs

International comparisons increasingly underline the growing gap which exists in ICT provision against cutting edge education systems internationally. The EU Eurobarometer Survey of ICT in schools (2002) shows that Ireland is under the EU average for pupil to computer ratios (EU avg. 9:1) with the leading countries averaging as follows : Denmark 3:1, Finland 6:1, UK and Sweden 7:1. Ireland averages 10:1. Ireland is last in the EU in the provision of broadband connectivity within schools (0%), the EU average is 32% with Sweden, Denmark and Finland at 60% or above and the UK (where there is a commitment to 100% broadband provision by 2005) at 27%. Neither is it a co-incidence that the high ranking Nordic/Scandanavian countries are also the most technologically advanced and most profound users of ICT. Investment in ICT for the future Substantial funding will be required in the years ahead in the following broad areas: ▪ To provide schools with the necessary equipment, networks and support, including technical maintenance ▪ To ensure broadband connectivity to the classroom ▪ To enhance teacher proficiency in ICT managed learning ▪ To integrate ICT in the curriculum and provide digital resources for use in the classroom Broadband in schools The ‘always on’ nature of broadband connections allows school students to use the internet more easily as an everyday teaching, learning and research tool in the classroom. High bandwidth also enhances the effectiveness of classroom learning Schools need access to an information technology infrastructure including high levels of connectivity at an affordable price. Broadband is required in schools :

Digital Literacy The global knowledge society requires an additional range of life skills if each individual is to fully participate in and benefit from the new digital age which now emerging. The digital divide is not just about those who have no access to technology but about those who do not have the skills to use it effectively. We must ensure that our young people, especially those in disadvantaged areas, are provided with all these skills in their schools and that learning is made more attractive leading to greater educational achievement. Digital technologies and their applications have the potential to make learning exciting and highly participative. The provision of content-rich, user-friendly digital resources for teaching and learning will be a key requirement if this potential is to be fully realised. By digital literacy we mean that citizens can intelligently use technologies, such as the Internet to locate appropriate content, but more importantly, that they can creatively produce their own content in a digital format – whether it be a Web page, a piece of computer-assisted art, a digital radio or video programme or their own multi-media composition. Digital literacy is much more than the ability to read and write. It includes the ability to intelligently read all types of visual and aural information and to actively communicate ideas in visual formats; the ability to find and evaluate information and the skills to communicate ideas in visual and other formats. The innovative use of digital technologies is a key challenges facing education for the future. It provides opportunities for creativity, collaboration and expression – individually or in groups. It will help to unlock the unique individual potential to shine which every student possesses. Digital media has the potential to make learning exciting and highly participative. It allow us to be creative and active producers of digital content on an individual or team basis. One of the reasons that the computer games industry, an industry bigger than the film industry, has grown so rapidly is that the newer games allow the user to engage in character and narrative development and environment creation. The player becomes the creator. In general, the provision of rich interactive resources through broadband will provide schools with an unique opportunity to develop new classroom strategies for learning and teaching – one where cross-curricular learning takes place at the pupils own pace and learning style. Pupils will learn and practice higher order skills at a younger age and individualized learning will be enabled. Learning will be participative and collaborative.

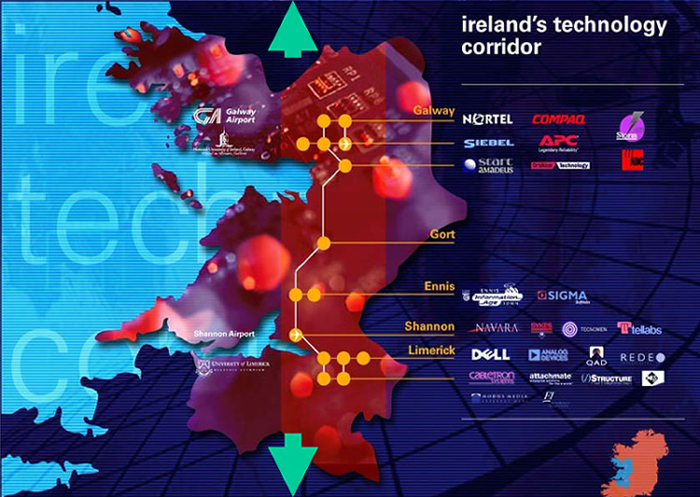

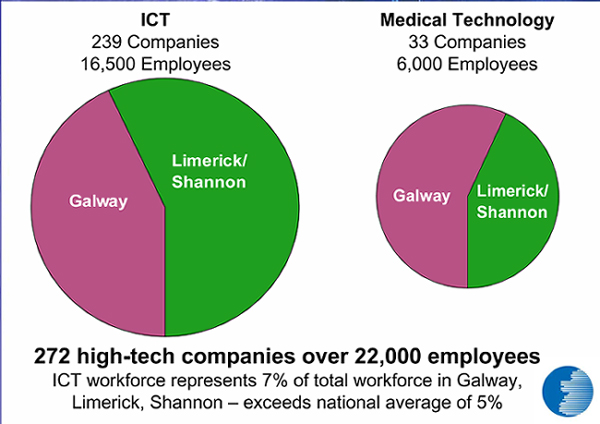

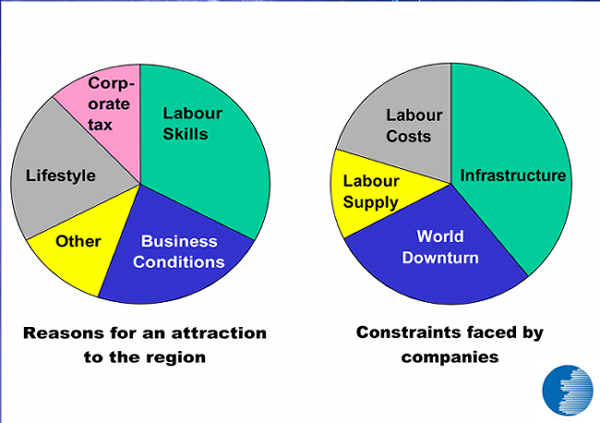

Atlantic Technology Corridor Building a World Class Technology Cluster

ATC Advisory Board

– Mike Conroy, Nortel Networks – Noel Fogarty, Boston Scientific – Chris Coughlan, Hewlett Packard – Reginald Freake, Dell Computers – Kieran MacSweeney, Avocent – Michael Byrne, Ennis Information Age Services – Gerry Joyce, Chorus & ShannonSoft – Seamus Kilbane, NetIQ & ITAG – David Silke, Nortel Networks – Cyril Burkley, University of Limerick – Roy Green, N.U.I. Galway – Kevin Thompstone, Shannon Development – Emmanuel Dowdall, Western Regional Manager, IDA – Seamus Bree, Enterprise Ireland – Jim Keogh, Udaras na Gaeltachta – Mike Foley, Shannon Development Cluster Profile

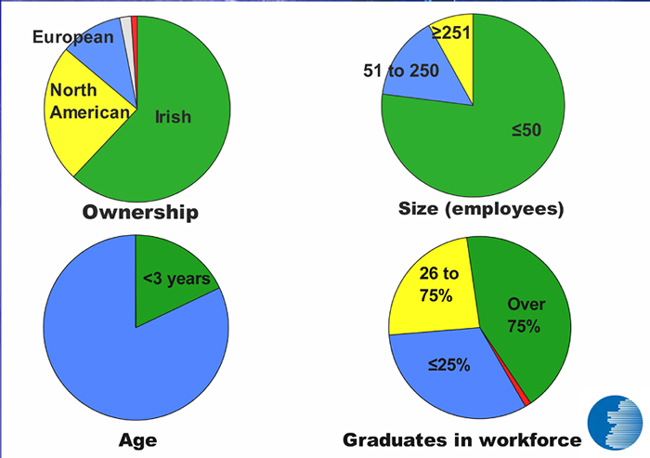

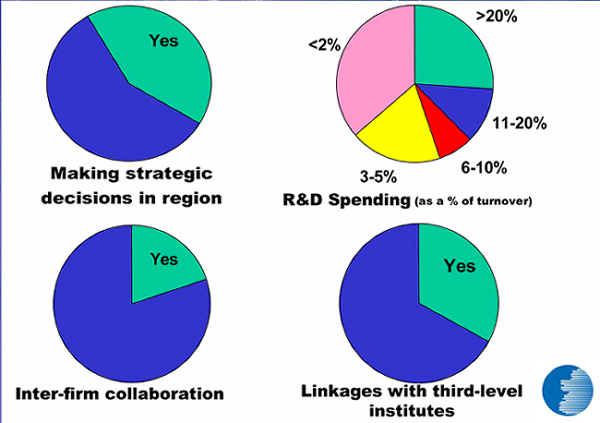

Characteristics of an Emerging Cluster

The ATC ChallengeBuild a world class technology cluster

– counter balance to east coast cluster. Cluster Profile

Opportunities and Constraints

Common Issues for Technology Companies

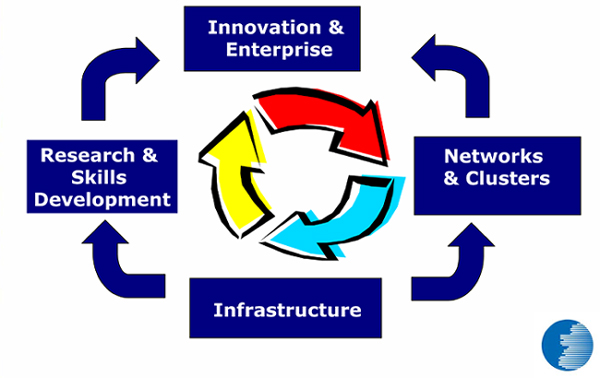

…The Four Pillars…

ATC Broadband Infrastructure

ATC Cluster Priorities

Call to Action

– MNCs <> SMEs – Industry <> University research – Development agencies. Broadband: Reducing the gender and other Socio-Digital Divides Experience, Education, and Effect By Frances M Buggy, MBA – Business and Government technology consultant. A presentation to the Joint Oireachtas committee on Broadband, July 2003 Most inequities, including those of gender, opportunity, and education - apparent in the digital world, are due to socio-economic factors and socio-cultural expectations that apply generally, rather than to any particular characteristic of the technology itself. This is borne out by the work of many analysts including Proff. E. Trauth of PennState University. http://www.ist.psu.edu Women are among the many disadvantaged groups when it comes to accessing the Internet in the optimum way. Ideally access should not be by dial-up – the “demand killer” as evidenced by relatively stagnant Irish Internet access rates; but by affordable high speed always on connection delivering decent bandwidth experience at all hours of the day 7 days per week. The primary reason for this gender disadvantage is because in Ireland technology is normally accessed first and fastest, in the workplace, where women are under-represented. This under-representation is further compounded by the disproportionately low number of women in the technology facing sectors of Science, Engineering and ICT study disciplines and resultant careers. The manner in which one accesses the Internet greatly influences ones usage patterns – home based access is primarily dial-up access at realistic Irish speeds of around 33 on a 56k modem. This method of access inhibits and often prohibits the key activities of the Internet – search, appreciation of the structuring of information, online collaboration, audio-visual shared learning The bridging of this predominantly urban/ rural, male/female, educated/uneducated, and single/family based digital divides will be broadband enabled but fuelled by the stimulation of an appetite for education and advancement among under represented groups, and by parents for their children. In society, women are generally community builders and usually passionately interested in the education of their families - these two behavioural factors can be leveraged when women in communities, and as parents are targeted and encouraged to get involved in learning more about using the internet to ensure that with their guidance, their children and their communities can compete effectively. Broadband, through the provision of secure high speed remote access to the work and educational infrastructure can also be used by these same women and men to facilitate upskilling and re-entry to their careers following a parental career break; and reduce the pressure to choose between parenting and a career. This should increase the retention and progression of skilled qualified women in SET, whose numbers are already at a low base. These findings are supported by the Greenfield Report, commissioned by the DTI/UK government to address how the UK economy can ensure it fulfils its innovation potential through the retention and induction of Women into Science Engineering and Technology. Dr. Lucy Cusack of Forfas has initiated a similar examination process for Ireland Some objectives of this presentation

Some General Usage Inequities and constraints: If users are caught in a bandwidth bottleneck as is common especially in the indigenous SME sector – it has been proven that they will negatively amend their behaviour, and if the bottleneck no longer exists – they begin to fully exploit the technology, and become more cost effective, competitive, more creative, and more innovative. 2/Conference organisers are very confined by high event-related communications costs and negligible bandwidth, which inhibits the international exchange of real time, shared learning by live audio visual conferencing for example. E.G. Due to communications unreliability in a range of venues throughout the country including Dublin, in over 5 years of running Irish and International events with the IIA – we never once used live infrastructure to deliver presentations or content – it was always from a stored file on a CD Spatial Planning and Budgeting

Supply Driven RolloutIt has become obvious since deregulation in 2000 that Ireland cannot depend on Telecoms companies or demand drivers alone to deliver broadband. To have demand one must:

It is valid to compare the transformational effect of widely available affordable broadband, with that of the last major Supply driven rollout: Rural Electrification –a scheme that revolutionised Ireland in the past, Affordable available Broadband will have a MORE transforming effect

Broadband infrastructure and the telecoms market Eircom and BT/Esat will act only on a business case basis, and on energetic compulsion by Comreg, and the Competition Authority. Their “2 Telco waltz” around the regulatory environment, has deferred their need to invest, and has cost Ireland its advantage over emerging Eastern European countries. (See comparative cost and performance tables on http://www.irelandoffline.org) I applaud the efforts of Min Aherne and ComReg regulator Etaine Doyle in this regard to date. Some infrastructural recommendations- True competition drops price and increases access – Support ComReg and the Competition Authority in their efforts to ensure real competition in the marketplace, and actively encourage Eircom to wholesale single billing, and realistically and economically unbundle the Last mile of copper into Irish homes. - In this way, so the home or small office user can reduce the access bottleneck and pre-select any carrier by bandwidth availability, quality of service, cost effectivess; and availability of single billing. Line Rental /Multiple billing and modem adjustment requirements are effective barriers to entry for residential users, and residential users yield a lower return than business users so until comparatively recently – telecom companies were content to argue about LLU rather than work to change it. - M.A.N management company (MSE) should be an expanded resource almost like the Treasury Management Agency – but be a National Network Management Agency, and have entitlement to confidential access to full information from commercial carriers as to infrastructure roll out and usage, to avoid further shameful duplication and allow the National Network to avail of other infrastructural build opportunities. - MAN – look at innovative rollout mechanisms which might save money and allow for interconnection of the MAN rings – and the ability to charge private carriers using the infrastructure, to defray the cost - Broadband is Not just DSL – reality of access is required rather than an aspirational press release – e.g. 88 out of 440 exchanges are supposedly DSL enabled, but in reality only some of the exchanges quoted in advertisements can currently deliver broadband, and even then – only to within 2.5km of the exchange. - Because broadband is not just DSL there is a need to focus on the solutions for locations which are 2.5 KM or more away from the nearest DSL-enabled exchange, as the Irish population is dispersed throughout rural areas and in urban clusters of insufficient scale to command the urgent interest of a telecoms company. E.g. Hotspots/ Wireless LANs, broadband VPN’s, Satellite enabled asynchronous access, splayed access for business and community users enabled by the MAN rollout. - ComReg need to continue to exert pressure on: LLU rates, single billing of all services, FRIACO, and encouraging the aggressive rollout of smaller competitive services – satellite enabled, fixed wireless etc – combinations which have an enabling effect on existing infrastructure. Demand stimulation:It is essential to take an omnipresent supply model approach to broadband provision, but develop value added demand driver services in parallel. These demand drivers could be funded through – co-ordinating public/private submission of Interreg, FP6 eTen Telecom and eContent funded projects of National and Regional significance, before we lose our 75% funding status in 2006 (Objective 1 in Transition) [The experience I have gained - working with National stakeholders at regional level to resolve ICT issues of National and regional importance leads one to believe that the South-East Information Society Strategy a 6 county project in the SE - is Ireland in microcosm.] Demand drivers include: 1/eTailing: 1. The active visibility critical mass of retailers and service providers on the Irish marketplace which could attract large volumes of consumer and SME transactions, 2. Actively driving Irish users online through improved service levels and discount incentives only available online, together with effective budgeted integration of online media in the corporate marketing mix/media schedule. A cursory glance at UK TV advertising provides evidence of the contrast in approach by retail and service providers serving the UK versus the Irish market - most Irish advertisers don’t have an electronic marketing budget and many don’t even quote their web address! 3. Relevant online services which stimulate interest whether one is male or female: eLearning/blended learning, Work Life Balance/eWorking; eHealth, eGovernment services, eBanking with more competitive offers online. 2/e Health: The primary care and diagnostic sectors could be revolutionised, taking pressure off the hospital sector and facilitating faster diagnosis, better aftercare, and more effective patient care in their own homes – where they want to be. E.g.

3/eGovernment service development: Certain eGovernment services depend on National deployment from Departmental back-end systems – however a different non-centralised approach is required at local government level. One which focuses on the on the transaction/knowledge management capability development of services from individual local authority back-ends, using process mapping, increased standardisation of database and firewall formats, rather than on what the front end forms will look like. A Possible focus on local back ends, potential data-mining, and common process mapping as developmental drivers – by CMOD & LGCSB & rollout in pilot regions – eg the six local authority IT departments in the South-East already work closely together in this regard and would be an ideal site for pilot trials. EGovernment should be about enhancing and re-inventing the relationship with the citizen – not just automating it. Also work to make eGovernment content relevant to every citizen instead of being an expression of organisational administration – the OASIS website is a good example of this approach – it is organised around Life events rather than departmental administration. 4/eLearning: The current approach Nationally, appears to be characterised by too much fragmentation, and a lack of “joined-up” thinking by policy makers and those in charge of 3 rd level bodies This lack of a shared National platform can create a situation where Institutes of technology and Universities are effectively hostages to fortune in terms of high-ticket renewable campus licences and duplicate implementation charges from primarily 2 US/UK based eLearning companies. A National eLearning platform co-ordinated by HEA might have combined the provision of global best practice in a manner which minimised licence cost and optimised shared organisational learning, and both indigenously and internationally provided functionality. Lifelong blended learning will be the key to National and industrial continuous improvement, increased competitiveness, and the facilitation of career change among disadvantaged groups in Ireland A 36% drop in secondary school leavers is envisaged in the short to medium term; and this should concentrate the minds of those running bodies of Higher education of the need to focus their efforts on more easily distributed Blended Lifelong learning without any perceptual bias against non-traditional methods of delivering undergraduate or postgraduate programmes. PHD and Executive MBA programmes are among the kind of programmes, which lend themselves to this kind of blended delivery; the third level sector in Ireland must now compete with the top “Ivy league” in the US and Europe – who can sell their strongly branded, and prestigious educational offerings worldwide – using broadband enabled computer mediated environments. Education: While education is a demand driver for Broadband, it is also crucial to look at how our education system is performing in terms of the creation of adequate numbers of male and female students pursuing careers in the key science engineering and technology sectors. The HEA reports show the disproportionate involvement of urban rather than rural lifelong learners, and male rather than female students in disciplines of national economic significance, which are natural usage areas for broadband enabled collaboration and R/D – Science Engineering and ICT technologies. To reverse some of these trends, which underpin the digital, and SET divide, some educational initiatives are essential: 1/Active SET Careers Guidance Intervention is required with final year primary/First year secondary school students in co-ed and Girls only schools by well-briefed career guidance teachers and guest speakers from a county-by county mentor panel of women who have built careers in Science Engineering and Technology. (SET) (Ref. www.witsireland.com talent bank) This intervention should be aimed at influencing informed subject choice as early as possible – so that Mathematics, Physics, and Chemistry are available, demystified and chosen as subjects throughout second level, especially by girls. Possibly suggesting an approach to Business careers through a more balanced pursuit of graduate SET degrees and post-graduate business degrees. 2/Extra points could be allocated to these SET and R/D enabling subjects, as in the past with Irish – to encourage choice and retention to Leaving Certificate. 3/Extra curricular and inter-school activities which focus on these subject areas should be encouraged and funded through public-private partnerships between government, academia and relevant regional and industry groupings 4/Educational infrastructure should be actively designed to facilitate shared learning and collaboration – E.g. HEANET running professionally managed networks at secondary as well as third level; – Implement wireless LAN’s of student laptops to encourage informal clusters of computer mediated activity; – Change from desktop to laptop provision at secondary level to increase the computing lifestyle of students and ensure that the student’s family are encouraged in their involvement with the laptop enabled online access to homework resources. – Move existing desktops in secondary schools to the primary sector so that children learn to play with technology before they develop any “received” learning barriers – Ensure that each school is a wireless hotspot which can recoup funds through splaying its signal to neighbouring commercial or community organisations not on the public MAN – Re-design school insurance and staffing arrangements so that their community can avail of school broadband access after school hours for community training or development initiatives. 5/ Certified Lifelong learning and career conversion strategies, need to be delivered in a Blended fashion (offline and online) to facilitate:

Work-Life Balance/eWork: Use broadband as an enabler of Work-Life balance for both men and women – so that part of ones working week does not involve commuting, facilitates intensive periods of quiet research and administration from home or preferably from ones nearest dedicated eWork centre, and access to high bandwidth resources for career development, lifelong learning, and collaboration in virtual teams. Ework and Flexible working: Clustered rather than home based eWork solutions need to be provided at entry and senior levels for very different but compelling reasons. These clusters should be supported by all the public and private regional stakeholders, ideally located on the edge of every regional Campus of further education or in dedicated rural catchment centres – so that quality broadband access can be associated with the economically essential activity of shared lifelong learning, secured remote access to the corporate environment and community involvement, rather than any one private company, government agency or regional stakeholder. The positive effect of this cluster phenomenon, especially for women re-entering their careers, is borne out by various studies in Flexible working e.g. (www.flexwork.eu.net), and the experience of community groups who have made a great success of any of the CAIT (Dept. Environment) funded initiatives. 1. eWork needs to lose the association with low-income telecottage/part-time activity and needs to be appreciated by employers and staff alike as a life/career enhancing extension of the secure infrastructure of the workplace. 2. It is essential that the management of those availing of remote /technology enabled flexible work arrangements select motivated senior people from both genders irrespective of perceptions of their parental status. 3. MBO: Achievement of objectives should be uppermost in staff evaluation terms, rather than the current status quo of expectation of evidence of the employee’s presence over excessively long hours in a centralised office. 4. It is also essential that public or private sector eWork/Flexible working does not confine those availing of it to low status part-time work, nor does it preclude those availing of it from promotional opportunities. eLogistics and roadspace management Broadband enablement is particularly appropriate for Ireland, as we need to export more internationally tradable services and goods with a high value to weight ratio – i.e. goods with a significant service-wrap/ software/ service value-add. - Without this infrastructure for larger indigenous Irish industry, our GDP suffers, exports are depressed, and cost effective procurement of sub supply becomes merely an aspiration. - Broadband makes more effective supply chain management possible, and companies can focus on value add activities on a more competitive cost base. - In Ireland we have a disproportionate dependency on road transport, and a relatively poor road infrastructure. Broadband can allow one to locate and manage warehouses and stock movements in a manner, which optimises the available infrastructure, minimises road related delays, and improve the administration of delivery management. Among its many transformational effects, access to Broadband can make geography – into history.

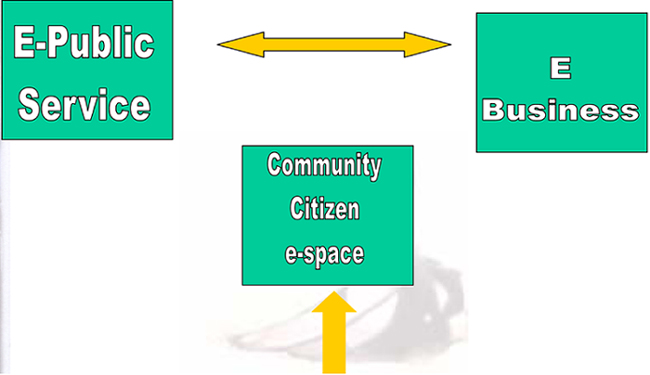

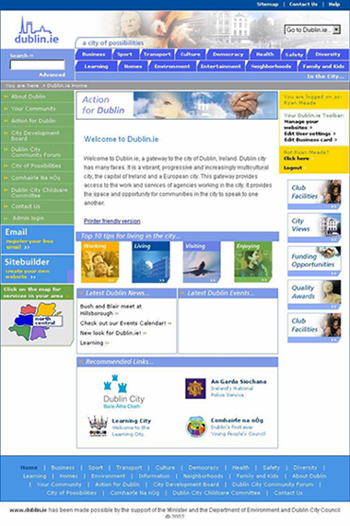

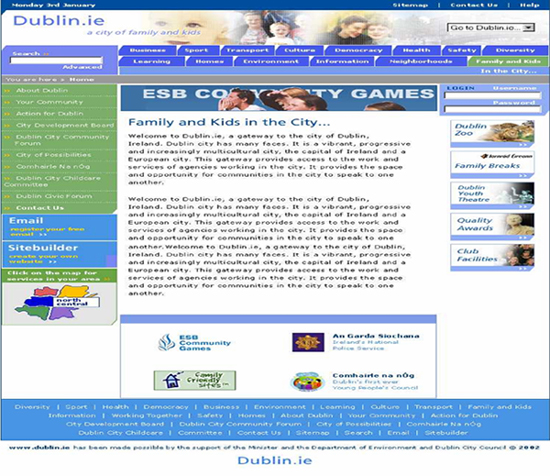

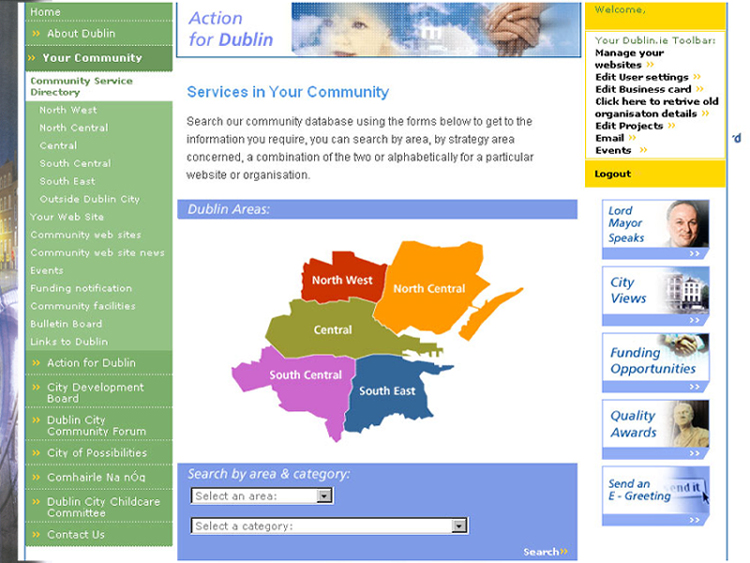

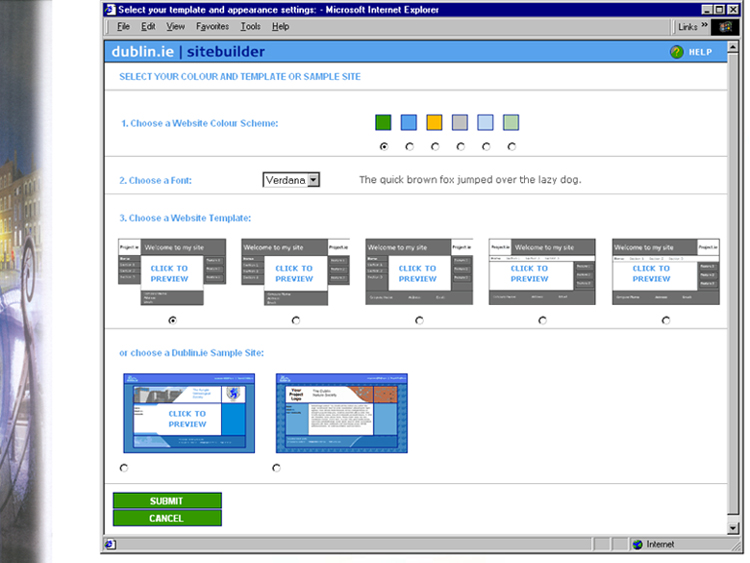

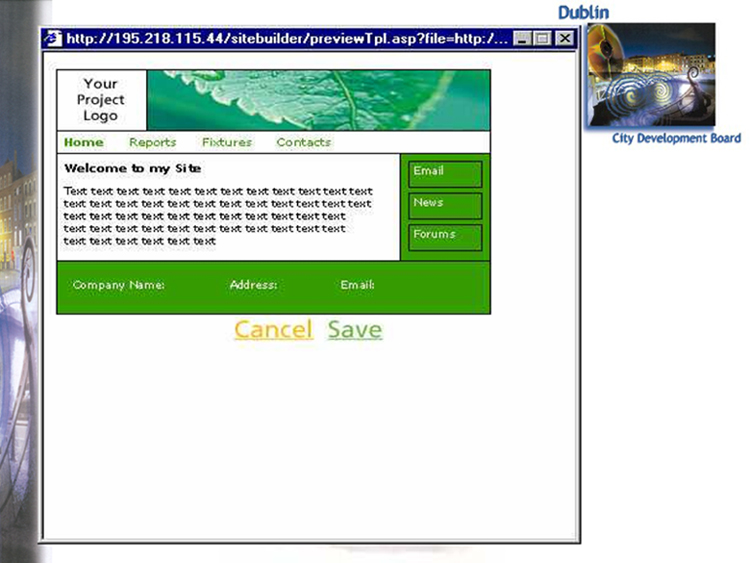

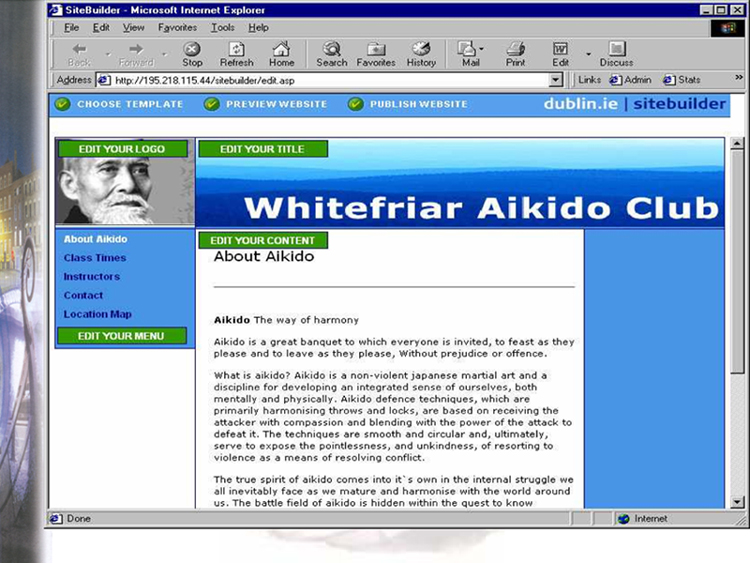

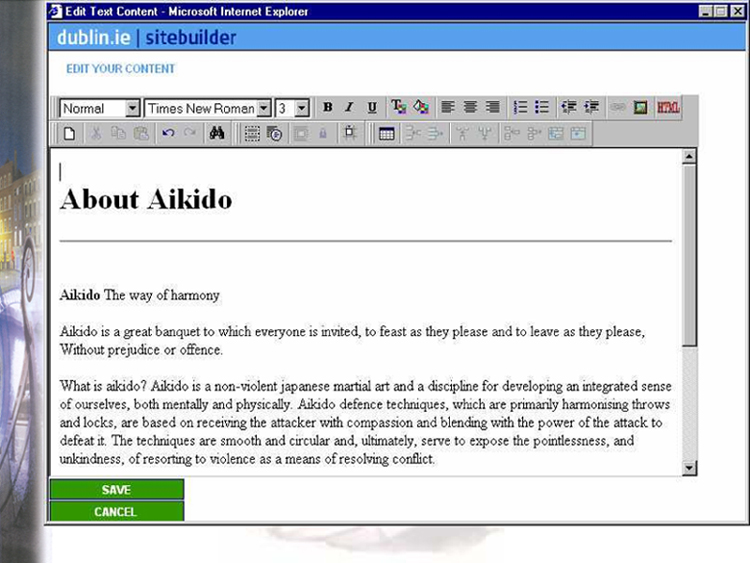

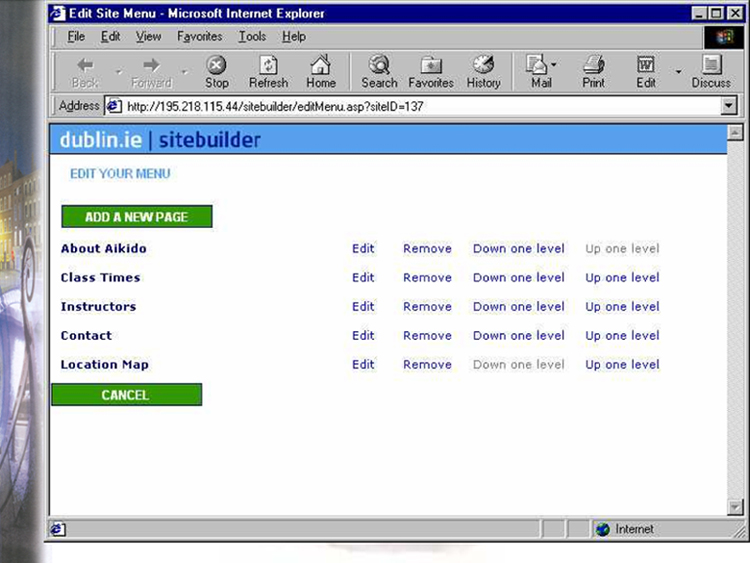

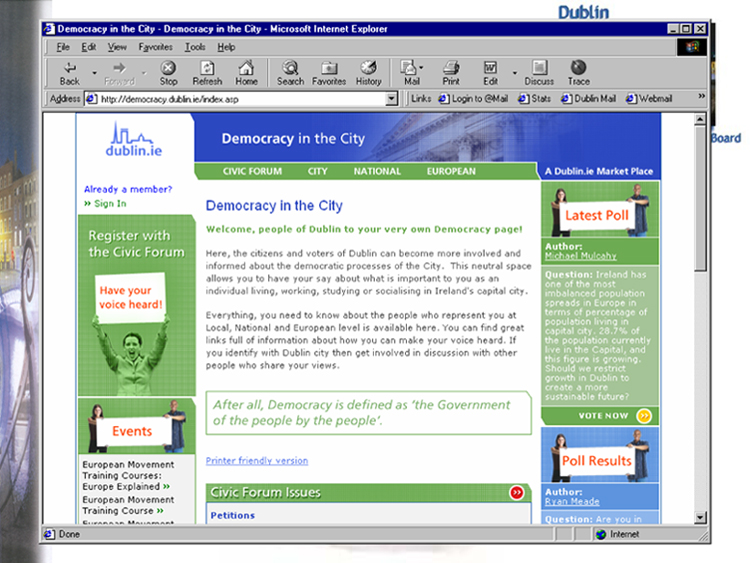

Citizens On Line www.dublin.ie: Creating an E based Community in the City www.dublin.ie - promoting the Dublin City Strategic Plan

What is Dublin.ie?

Dublin.ie - The Gateway to the City

Summary of the Project

In this project we are trying to create an audience in many ways: i) create online services relevant to the every day to day life of a city dweller. ii) use technologies that are within the culture and reach of everyone, e.g. TV access. iii) provide education and training in technology and the opportunity for community groups to participate.

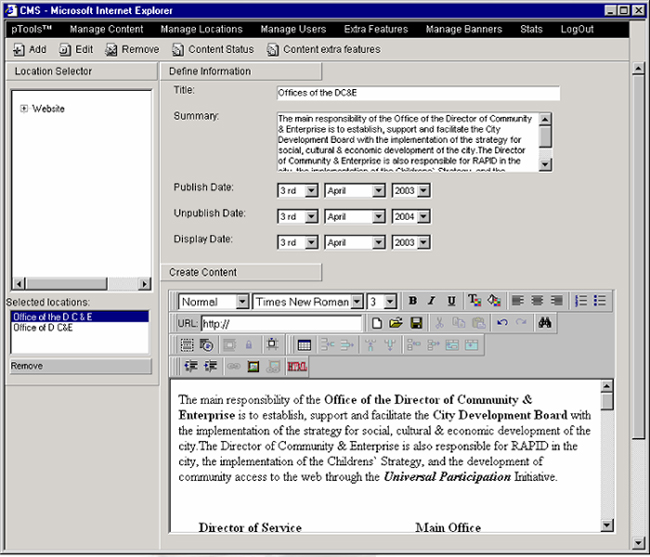

The Key is to develop a “content management system” which every user can use to update their content. Project Objectives

Why Communities on the web and how...?

What is available now on www.dublin.ie?

Coming soon to www.dublin.ie

New features on www.dublin.ie

Coming soon to www.dublin.ie

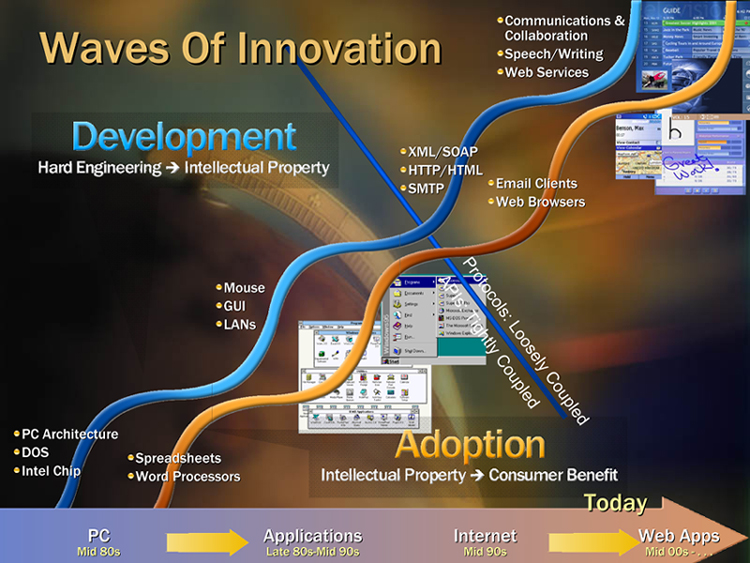

Future Potential Value of Broadband to Ireland Inc.Presented by Joe Macri, General Manager Microsoft Ireland to Oireachtas ICT Sub-Committee On Thursday, 5th June 2003 Proposed Agenda

Digital Decade

Realising Benefits

Source: The Payoff of Ubiquitous Broadband Deployment - Gartner Barriers to address

Recommendations

1. Discounts for disadvantaged people 2. Group purchase 3. Public IT literacy programme 1. Remote rural satellite service 2. Building certification scheme 3. Incentives for home PC adoption 1. Free broadband to schools 2. Extend teacher training 3. Internet as a resource for homework Questions?Thank You Microsoft® © 2003 Microsoft Corporation. All rights reserved. This presentation is for informational purposes only. Microsoft makes no warranties, express or implied, in this summary. Presentation to the Joint Committee on Communications, Marine and Natural Resources (ICT Sub Committee) 5th June 2003 Martin Murphy

Overview of HP in Ireland

ROADBANDNew Connections, the Government Action Plan on the Information Society, was launched in April 202. “It ambitiously sets out the Government’s Strategy to ensure that Ireland established itself as a world leading location for e-business and knowledge-based economic activity and that the benefits….are available to all Irish citizens”. “The objectives for Broadband infrastr ucture and services include: Making open-access affordable, always-on Broadband infrastructure and services for businesses and citizens available throughout the State, within three years. Broadband speeds of 5mbit/s to the home and substantially higher for business users as the minimum standard within ten to fifteen years”. Broadband Ireland Inc▫ Competitive Advantage ▫ Enables effective E-government ▫ Empowers Citizens ▫ Level playing pitch for all Regions ▫ Promotes Partnership Benefits▪ E-government ▪ Healthcare ▪ Education Social Value▪ Bridge Digital Divide ▪ Promote e-inclusion ▪ HP - Citizenship

Our Vision Philanthropy Using our IT expertise to deliver solutions that bridge the Digital Divide: We live up to our responsibility to society by being an economic, intellectual and social asset to each country and community in which we do business. HP bringing IT solutions to the Community in Ireland

Gender Aspects of the National High Speed Broadband InfrastructurePresentation to the Oireachtas Joint Committee on Communications, Marine & Natural Resources, sub-committee on ICT. Sadhbh McCarthy Gender Strategy in Broadband deployment

Gender equality and ICT policy

Gender Considerations

Gender Considerations- Access

Gender Considerations- Capacity and Skills

Gender Considerations - Economic & Social

Gender Considerations- Public Sector Policy

Opportunities - Social & Economic Equality

The Road Map....

Summary - where we are...Summary - where we can be….

Axia Ireland Broadband PropositionHow The Supernet Works Ireland’s Broadband SolutionNew Connections, the Government Action Plan on the Information Society, was launched in April 2002. “We wish to see Ireland within the top decile of OECD countries for broadband connectivity within three years.” “Axia's basic value proposition to government is: Ireland can have a ubiquitous broadband network for all public agencies and solve the rural service deficits for about the same annual cost they are already spending today!” Axia are implementing a similar solution for the Government of Alberta Who is Axia?

– Founded in 1995 – Toronto Stock Exchange listing – Excellent revenue growth throughout history How The Alberta Supernet Works

– The base network will link the province's 27 major urban centres. – The extended network links 395 more distant communities A six-megabit high-speed broadband connection can cost as much as $10,000 per month today - and service levels of this type are available only in major urban centres. By contrast, Alberta SuperNet will provide 20-megabit service to every government institution in the province for less than $700 per month. Services

Alberta SuperNet 4700 Service Locations 427 Towns and Villages How The Supernet Works

– These are key junctions throughout the grid – Private Internet Service Providers can link their local networks into the SuperNet, to take advantage of broadband access. – This system creates a competitive marketplace where telephone and cable companies, and new suppliers, will have equal access to SuperNet - which means they'll want to offer services to their customers at competitive prices. – accessing these PoPs and Meet-Me Facilities means that ISPs won't be faced with the daunting and costly task of laying cable from outlying towns to the nearest major urban centre – which will translate into reasonably priced Internet access across Alberta. (In fact, the SuperNet contract stipulates that rural and urban access rates will be equal.) Alberta’s Goals with SuperNet.Broadband

John Chambers Cisco CEO says an address about broadband; An important factor will be cooperation between a variety of agencies and the government, With high-powered bandwidth-hogging applications becoming more and more in demand (these include e-commerce, e-learning and supply chain management). Building the infrastructure from the top down will be crucial. "Remember- a half an hour of video is the equivalent of half a year of emails," says Chambers, stressing the need to be able to handle the heavy data, voice and video traffic demanded by today's consumers. But it isn't just transport that will be important. Studies have shown that enterprise CIOs want more than just a provider of transport- they want customized value-added services”

Connecting Albertans to the WorldArthur R. Price. Chairman and Chief Executive Officer Axia NetMedia Corporation

Where does Ireland Stand?

OECD Org for Economic Cooperation & Development Ranking of Countries: Internet Users

– but slow movement means Ireland is actually losing ground. Broadband

New Connections, the Government Action Plan on the Information Society, was launched in April 2002. “It ambitiously sets out the Government’s strategy to ensure that Ireland establishes itself as a world leading location for e-business and knowledge-based economic activity, and that the benefits … are available to all Irish citizens.” “The objectives for broadband infrastructure and services include: Making open-access, affordable, always-on broadband infrastructure and services for businesses and citizens available throughout the State within three years. Broadband speeds of 5mbit/s to the home and substantially higher for business users as the minimum standard within 10-15 years.” Broadband Stagnation

What is the Challenge?

What is the Solution?

– Develop the existing framework further – Government as Enterprise Customer – Adopt a similar strategy to that which is being successfully implementing by the Government of Alberta Methodology

– By Server Consolidation – Lower Telecommunications Costs – creates and manages “last leg” to link non-competitive markets to competitive markets – Establish Meet-Me facilities in competitive markets – Create Points of Presence (PoPs) in non-competitive markets – – optical wherever possible, wireless where optical is not appropriate – In competitive markets – buy services from carriers to connect government premises to Meet-Me facilities – In non-competitive markets – create (build) the network for local access to Points of Presence (PoPs)

Final Observations

– Axia will deliver a ultra high-speed connection to every town and village in Ireland What Would it mean in Rural Ireland?

The Regional Business Opportunity

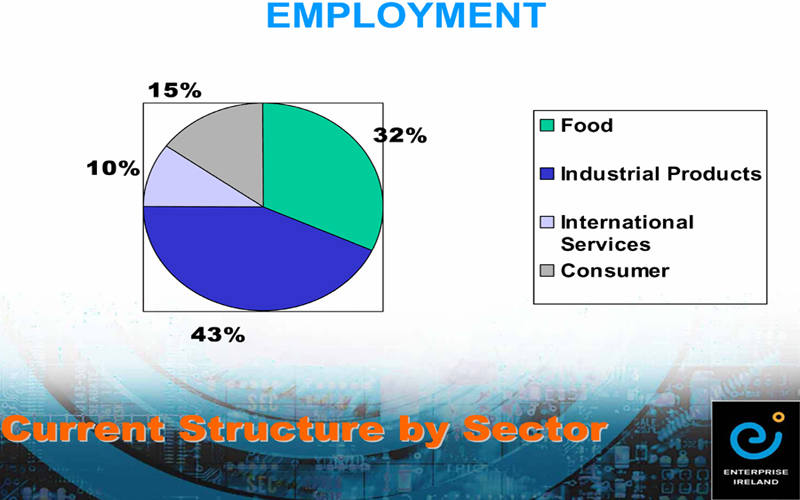

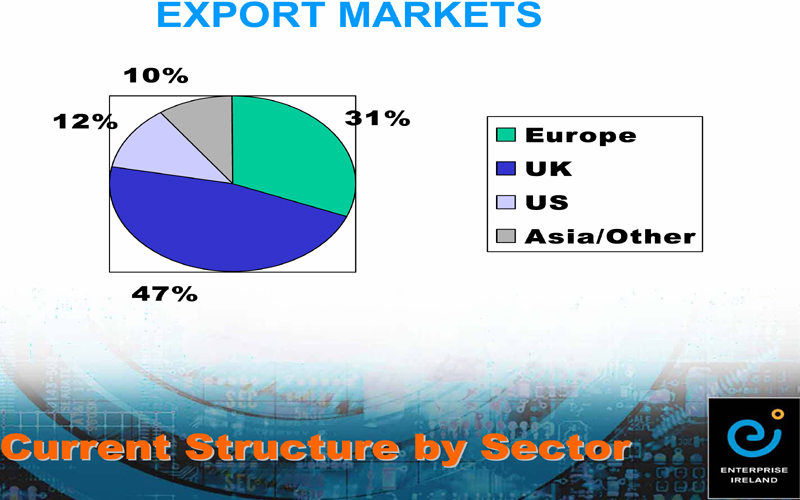

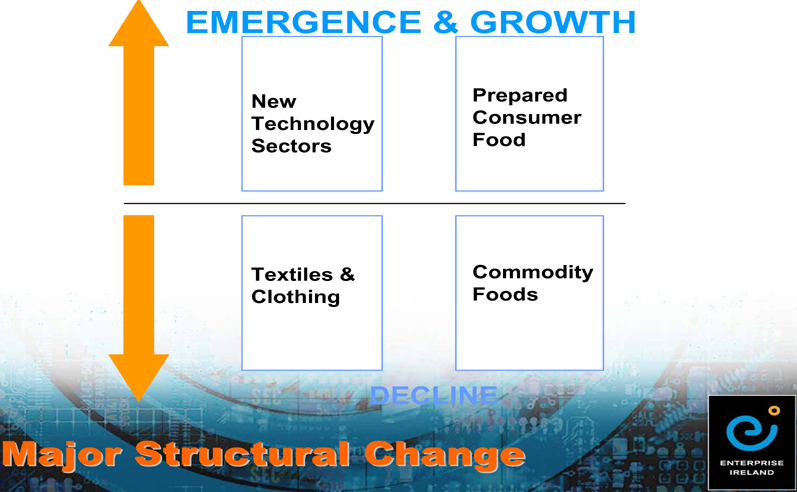

Joint Committee on Communications, Marine & Natural ResourcesICT Sub-CommitteeDan Flinter Chief Executive Officer Enterprise Ireland 24th June 2002

Agenda

Enterprise Ireland

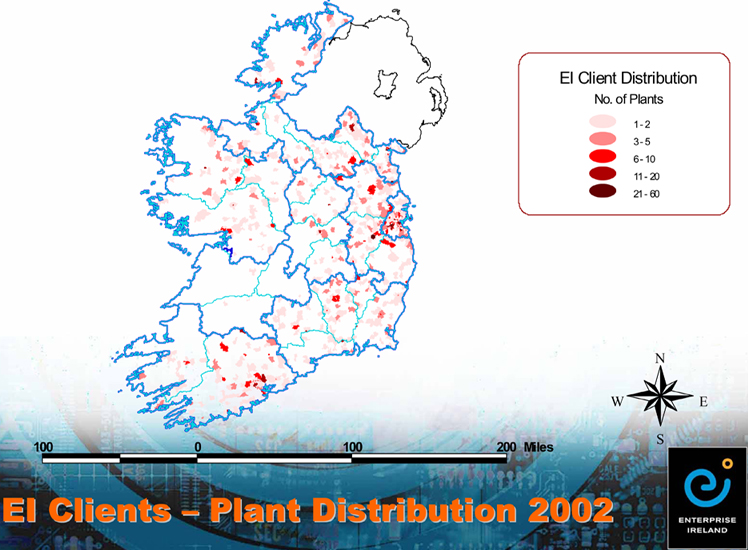

Enterprise Ireland Client Companies

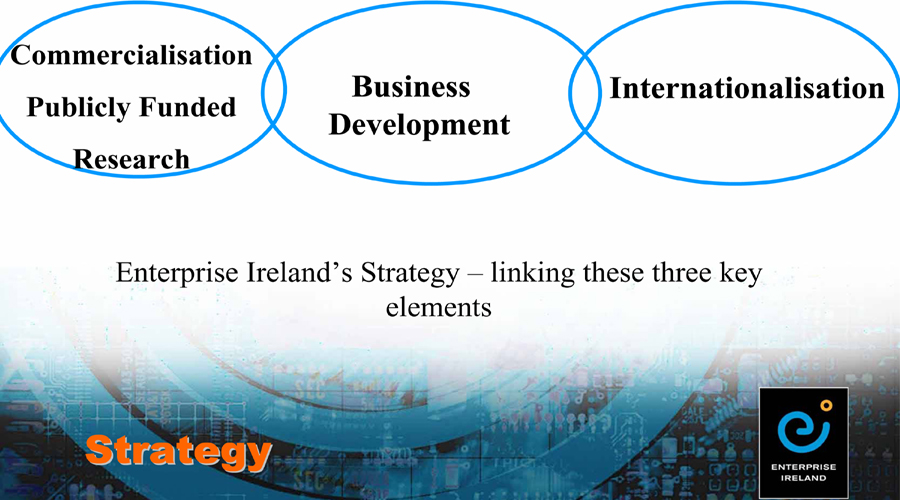

Enterprise Ireland’s Strategy – linking these three key elements

Telecommunications Infrastructure

– installation & operational

– lead times & technical support

EI Client requirements

Enterprise Ireland Initiatives

– Development of the National Broadband Backbone – Increasing number of nodes providing access into the Backbone – Development of local Broadband Networks linking into these nodes

Current EI Client Priorities Telecoms and Internet FederationPresentation to Joint Oireachtas Committee on ICT Sub-Committee

The Irish Telecoms Industry

Ireland’s Telecoms Infrastructure

Investment

Technology

Agendas

Provision of Broadband

Government Intervention

Broadband Deployment

Regulation in Ireland

while protecting Investment environment

Telecoms Regulation

ComReg

Pricing of Broadband

DSL - Progress

Source: Norcontel, Broadband Telecommunications in Ireland – Benchmark Study, Update Report March 2003. Vision Needed

Presentation to the Oireachtas Sub-Committee on BroadbandPeter Evans David Taylor 1st July 2003 Summary of Presentation

Who are Esat BT ?

What has Esat BT done ?

- Subscription services: Ireland On-Line, 1991 - Free services: Oceanfree, 1998 - Broadband Services: Esat BT ADSL, 2002 - Bundled off-peak Internet minutes: Netsmart, 2002 - FRIACO (Anytime) Service: IOL Anytime, 2003 Esat BT brings National competition

Alternative Delivery of Broadband Services

- Esat BT uses its own infrastructure - Esat BT is totally reliant on eircom providing wholesale services at the right price and right service level. Alternative Delivery of Broadband Services

- Esat BT uses its own infrastructure - Esat BT is totally reliant on eircom providing wholesale services at the right price and right service level.

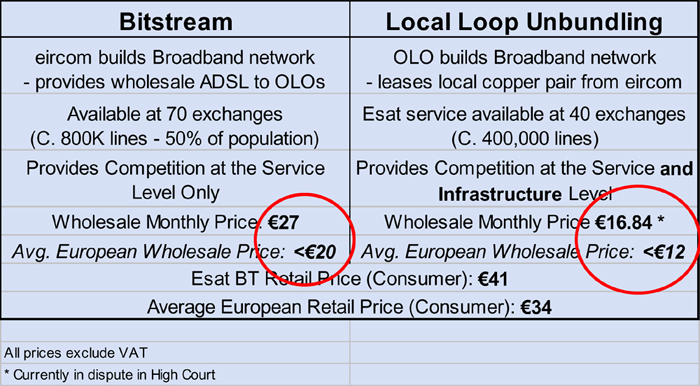

These 3 are inter-linked. Success only comes from low wholesale prices and high wholesale service levels. ADSL Services2 Wholesale Products are available to OLOs for DSL: Bitstream and Local Loop Unbundling

Roadblocks

- LLU charges under legal challenge. Eircom want €27 per month European average circa €12 per month. - Bitstream. Eircom charge €27 per month European average circa €20 per month. Driving Awareness of Broadband

- Current spend of €70 per week for 2 hours Narrowband (56K/64K) access. All paid to eircom. - Esat BT can deliver a combined Broadband/Anytime product for <€40 per month What can Government do ?

- needs to become a customer rather than a supplier of broadband services - Broadband rings will extend the reach of fibre, but will not address the final mile - access issues at wholesale level still exist. - Price stimulation: e.g. Subsidies, Low VAT for broadband ? - Clear Government mandate needed to ensure regulatory focus is placed on wholesale Broadband issues; price and service. - Greater urgency on the part of ComReg for LLU and Bitstream services. What can/will Esat do ?